What is a Capital Asset?

- All expenses can be classified into capital expenses or revenue expenses

- Revenue expenses are those which are incurred repeatedly over a period of time & the economic benefit is for a very short time

- Capital expenses are provide us with economic benefit for more than 1 accounting period (Eg: Furniture, Building, Air Conditioners, Plant & Machinery purchased can be used for more than 1 accounting period – hence these are capital expenses)

- Capital expenses are capitalised & carried to the balance sheet whereas revenue expenses are expensed off to the Profit & Loss Account

- Unlike the old indirect tax regime, which has strict definitions for what is a capital asset & which is not, under GST Law, any expense which is capitalised in the books of accounts is considered as a capital asset

ITC Treatment at the time of purchase of capital asset

- Same as Inputs & Input Services as discussed in the Common Credit Rules under GST document

What happens at the time of sale of capital assets?

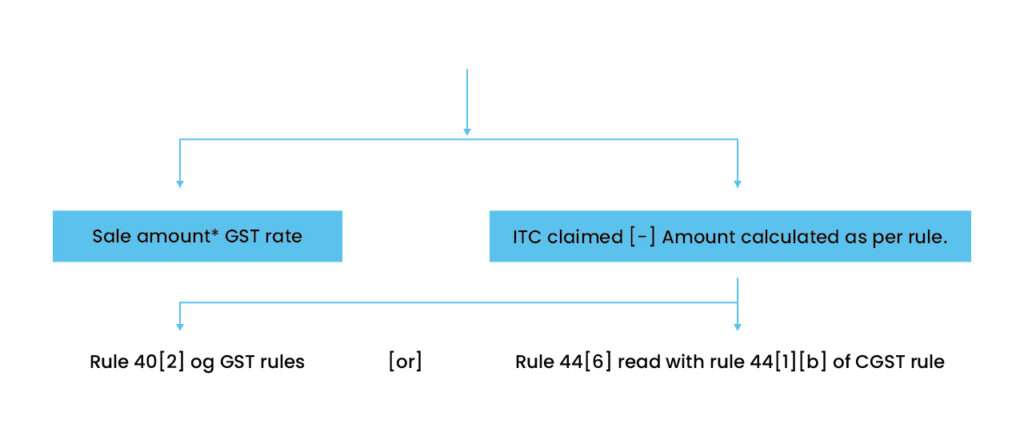

- If a registered person sells a Capital Asset used for business purpose, then tax shall be paid according to Section 18(6) of the CGST Act, 2017.

- As per section 18(6), tax should be paid on higher of the following.

ITC claimed *( 5% per quarter or part thereof ) ITC claimed * (used months/60 months)

Note 1. Part of months also treated as a month for Rules 44(6).

2. Useful life of the asset was 60 months as per Rule 44 of GST act.

3. Even if ITC was not claimed at the time of purchase ,GST needs to be paid on sale amount(Higher of the 2 Value). Because ITC claimed it was “Nil”.

4. Where refractory bricks, moulds and dies, Jigs and fixtures are supplied as Scraps, the taxable person may pay tax on the transaction value.

Not taxable in case of personal assets

For Example

Suppose, Mr X sold his Machinery for Rs.1,44,550 (Inclusive of GST at the rate of 18% of Rs.22050) on 10.05.2019 which he purchased on 01.07.2017 for Rs.2,36,000 (Inclusive of 36,000 as GST @18%).

| As per Rule 40(2), the amount to be determined is as follows: | As per Rule 44(6) read with Rule 44(1)(b), the amount to be determined is as follows |

| Machinery has been used for total 1 year, 10 months and 10 days which constitute 8 quarters | Machinery has been used for total 1 year, 10 months and 10 days which constitute 23 months. |

| Percentage amount to be reduced:8 quarters x 5% = 40% | Useful life left for use (according to CGST rules) is 37 months |

| The amount to be considered:=36,000-(36,000*40%)=Rs.21, 600. | The amount to be considered:=36000*(37/60)=Rs.22,200 . |

| Therefore the Amount payable is Rs.22,050 i.e. Higher of Rs.22,050 and Rs.21,600. | Therefore the Amount payable is Rs.22,200I.e. Higher of Rs.22050 and Rs.22,200. |