Expert verified

Expert verified Wondering how to save tax in business in India? We got you covered. Explore with us the best tips for saving taxes for businesses in India.

By implementing these tips you will be able to not only save taxes but also keep the most of your earnings for your business growth. We’ll cater to all kinds of businesses, small or medium and even growing and large.

How to Save Tax in Business Income in India?

Here are some of the best ways to save taxes for businesses in India:

1.

Identify & Claim Deductions on Business Expenses

To reduce taxable income, identify and claim deductions for legitimate business expenses such as rent, utilities, salaries, office supplies, and marketing costs.

These expenses, when properly documented, can significantly lower your tax liability.

2.

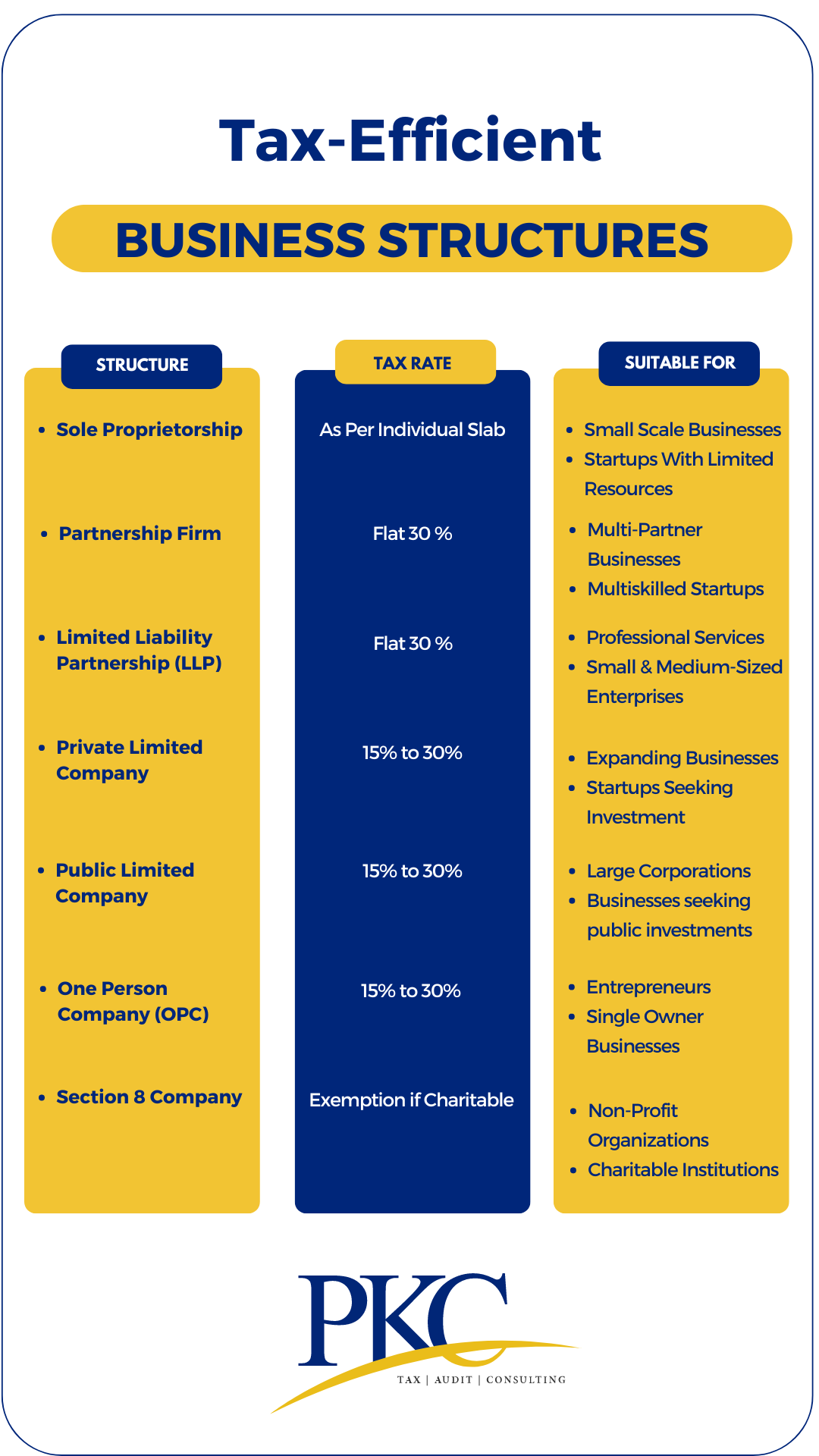

Opt for Tax-Efficient Business Structures

Different business structures have different tax liabilities. Choose a business structure such as sole proprietorship, partnership, LLP, company that aligns with your business and tax goals.

This is applicable for businesses who are just starting out or who are considering changing its legal form.

Also Read:

Tax saving tips for small business owners

3.

Claim Tax Relief for Depreciation

You can reduce your taxable income by claiming depreciation on assets such as machinery, vehicles, equipment, and buildings.

By systematically writing off the cost of assets over their useful life, you can reduce your taxable income and defer tax payments. Manufacturing businesses can claim additional depreciation under Section 35AD.

4.

Record Preliminary Expenses

This tip is suitable for businesses in their early stages. Keep track of all the money you spend before your business officially starts, like registration or legal fees, marketing costs, etc.

You can spread out these expenses on your balance sheets over a few years to reduce your taxes in the early stages.

5.

Invest in Tax- Saving Instruments

Invest in government-approved tax-saving instruments like Public Provident Fund (PPF), National Savings Certificate (NSC), or Equity Linked Savings Schemes (ELSS) under Section 80C.

You can use these investment opportunities to reduce business taxable income and avail deductions up to Rs 1.5 lakhs.

6.

Deduct TDS Where Applicable

Make sure you correctly deduct and pay the required Tax Deducted at Source (TDS) on salaries, contractor payments, and other specified expenses.

This not only keeps you compliant with tax laws but also reduces your taxable income.

7.

Save Business Taxes on Capital Gains

Capital gains are taxed differently based on the holding period. Reinvest capital gains from the sale of business assets into specified instruments like bonds or residential property under Sections 54EC and 54F.

Businesses can also reduce long-term capital gains tax liability by claiming indexation benefits. This is done by adjusting the purchase price of long-term assets like property or securities for inflation when calculating capital gains.

8.

Consider Engaging Professionals for Business Tax Planning

Consult an experienced chartered accountant or CA firm like PKC Management Consulting for expert tax advice and assistance.

With their expertise you can optimize your tax strategy and save money in the long run.

9.

Claim Expenses for Marketing and Advertising

All expenses related to marketing and advertising can be deducted from taxable income. This includes costs for:

- Digital marketing campaigns

- Print and online advertising

- Attending trade shows and conferences

- Promotional materials like brochures and flyers

- Hiring marketing professionals

By claiming these expenses, you can reduce your taxable income and lower your overall tax liability.

10.

Utilize Employee Benefits to Save Business Tax

Provide tax-exempt employee benefits like medical insurance, transport allowance, and housing allowance.

This will enhance employee satisfaction and retention. You reduce the taxable income of employees, thereby lowering the overall tax liability for the business.

11.

Save GST in Your Business

Businesses in India can legally save GST by planning strategically and ensuring compliance. Best ways to save GST for businesses is

- Maximizing Input Tax Credit (ITC): You can claim GST paid on business expenses like rent, advertising, software, and professional services, provided suppliers are GST-compliant and invoices are valid.

- Choose the right GST Scheme: For example small businesses can opt for the Composition Scheme with lower tax rates and simpler filing, though ITC isn’t available.

-

Correct Classification of Goods and Services: Under proper HSN/SAC codes prevents overpayment and penalties.

-

Plan your Supply Chain: Reduce interstate IGST, and claim ITC on capital goods like machinery or computers.

12.

Capitalize on Loss Carry Forward

If your business incurs losses, you can carry them forward to offset against future profits for up to 8 years.

Understand the set-off rules for loss carry forward to maximize tax benefits. This strategy helps in reducing tax liability in the profitable years.