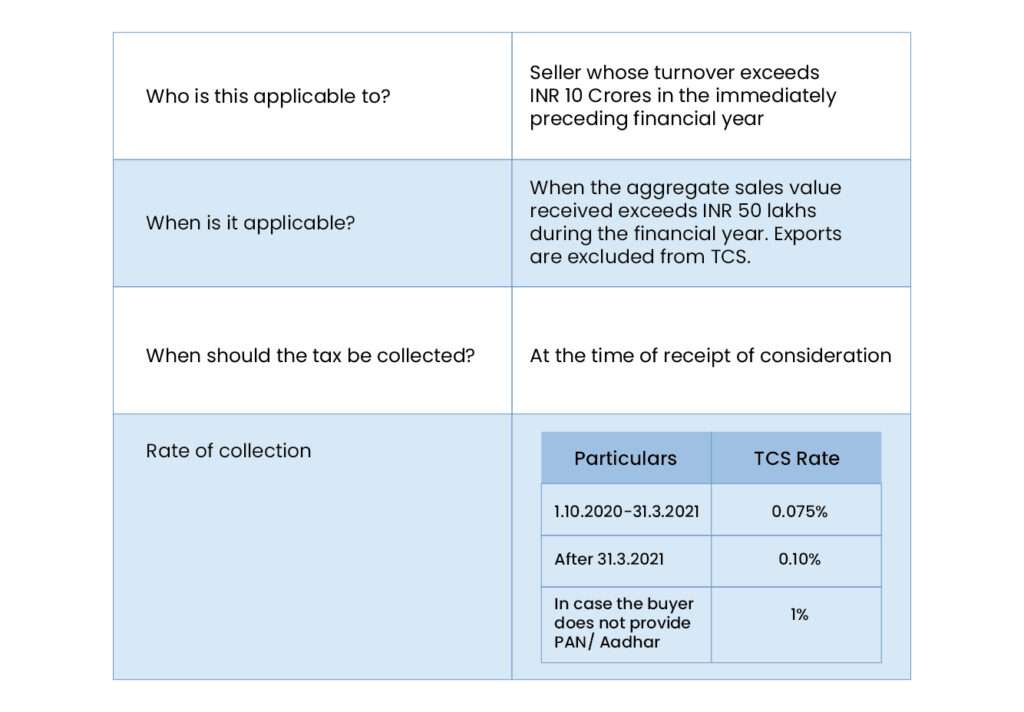

New IT provision w.e.f. 01.10.2020 to collect TCS on sales of goods above Rs. 50 lakhs

Example: Suppose M /s ABC Ltd. has turnover of Rs 20 crores in FY 2019-20 and has made sale of goods to Mr X of Rs 65 Lakhs in FY 2020-21 and receives Rs 52 lakhs as payment on 31.03.2021. What is the amount of TCS to be collected?

M/s ABC Ltd needs to collect TCS on the amount exceeding 50 lakhs i.e. (Rs. 52 lakhs – Rs. 50 lakhs) = Rs 2 lakhs* 0.075% which equals to Rs. 150 and file statement of such tax collected in Form 27EQ (TCS Return).

FAQs on TCS :

- What is TCS?

Tax collected at source (TCS) is the tax collected by the seller from the buyer at the time of sale or receipt of consideration. The TCS collected by the seller will reflect in Form 26AS of the buyer as a tax credit.

- How to collect TCS from the buyer?

The seller needs to raise the sale invoice including the amount of TCS, then account in the books as a TCS liability though the liability does not arise at the time of sale.

The liability crystallizes only when the amount is collected from the buyer.

- Under what situations, provisions of TCS on sale of goods will not be applicable?

If the person is liable to deduct TDS or collect TCS on the given transaction under any other provision of the Act and has deducted/ collected such amount.

- Should TCS be refunded in case of sales returns?

No, only the amount relating to sales should be refunded as TCS would already have been paid by the seller. However, if the amount is settled post adjustment of return, then on net consideration TCS should be collected.

- Should TCS be collected on the sale amount including or excluding GST?

The word ‘consideration’ is not defined in the Income Tax Act. In our opinion, going by the Valuation Rules in the GST Act, TCS should be collected on the amount inclusive of GST.

- What are the consequences of non-compliance?

- Levy of Interest: If the person responsible to collect TCS does not collect or after collecting fails to pay it to the Central Govt, then such person shall be liable to pay simple interest @1% per month or part thereof on the amount of such tax from the date on which such tax was collectible till the date on which such tax was actually paid.

- Levy of Penalty: If the person fails to collect the whole or any part of the tax, then such person shall be liable to pay a penalty which shall be equal to the amount of tax which the person failed to collect.

- Prosecution: If a person fails to pay to the credit of the Central Government the tax collected by him he shall be punishable with rigorous imprisonment for a term which shall not be less than three months but which may extend to seven years and with fine