Expert verified

Expert verified A Secretarial Audit in India ensures that businesses are following laws and standards. If ignored, may face heavy penalties, and legal trouble.

Understand with us all about secretarial audits for companies, their applicability, process and a checklist to help you get started.

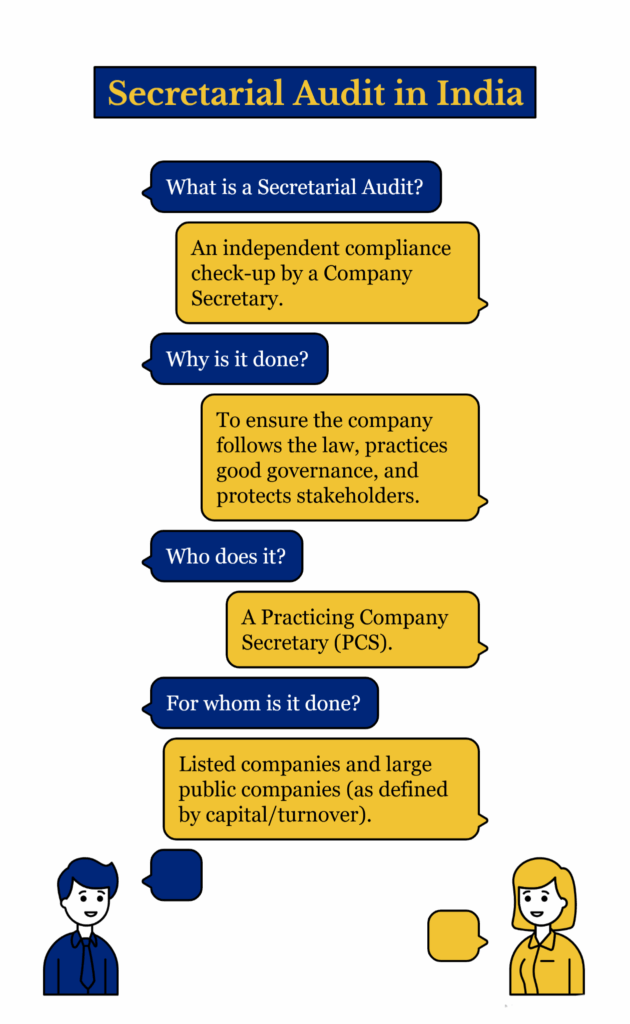

What Is a Secretarial Audit in India?

A Secretarial Audit in India is an independent compliance audit conducted by a Practicing Company Secretary (PCS).

It is done to verify whether a company complies with the Companies Act, 2013, and other applicable legal and regulatory frameworks.

A Secretarial Audit focuses on non-financial statutory and regulatory compliance, corporate governance processes, and adherence to legal procedures.

Objectives of Secretarial Audit

Ensure Statutory and Regulatory Compliance

- Verifies adherence to multiple laws, rules, and standards

- Helps avoid penalties, litigation, and disqualification of directors

Promote Good Corporate Governance

- Ensures transparency, accountability, and ethical decision-making

- Strengthens Board processes and documentation

Mitigate Legal and Compliance Risks

- Functions as an early warning system to detect procedural gaps

- Prevents serious compliance failures before they escalate

Protect Directors and Officers

- Directors are legally responsible for compliance

- A Secretarial Audit report serves as evidence of due diligence, limiting personal liability

Improve Investor Confidence

- Enhances trust among shareholders, potential investors, and financial institutions

- A clean audit report is often seen as a sign of credibility and sound management

Facilitate Strategic Transactions

- Assists in mergers, acquisitions, and fundraising by offering a clear compliance history

- Acts as a due diligence document for external stakeholders

Secretarial Audit Applicability: Private, Public & Listed Companies

Secretarial Audit in India is a mandatory compliance requirement under:

- Section 204 of the Companies Act, 2013

- Rule 9 of the Companies (Appointment and Remuneration of Managerial Personnel) Rules, 2014

It is designed to ensure that companies operate in accordance with statutory and regulatory frameworks. However, not all companies are required to undergo a Secretarial Audit.

The applicability of Secretarial audit for private companies and others depends on its type, financial size, and its association with listed entities.

Here’s a quick look at the eligibility of Secretarial audit for companies in India:

| Company Type | Applicability | Criteria |

| Listed Company | Yes | All listed companies, regardless of capital or turnover |

| Public Company (Unlisted) | Yes (if criteria met) | Paid-up capital ≥ ₹50 crore, OR Turnover ≥ ₹250 crore |

| Private Company | Yes (in specific cases) | If it meets the same financial criteria as public companies If it has borrowings ≥ ₹100 crore If it is a material subsidiary of a listed company |

| Private Subsidiary of Public Company | Yes (if parent meets criteria) | Treated as deemed public company for compliance purposes |

| Material Unlisted Subsidiary | Yes (under SEBI LODR) | Indian subsidiary of listed company with ≥10% of consolidated income/net worth |

Listed Companies

Secretarial audit is mandatory for all listed entities. This is because SEBI mandates higher governance standards for listed entities to protect investors and ensure transparency.

It includes all companies listed on any recognized stock exchange in India (BSE, NSE, SME platforms).

- Applies to both public and private listed companies.

- Listing increases regulatory scrutiny, especially under SEBI and stock exchange norms.

- Must obtain and attach a Secretarial Audit Report (Form MR-3) with the Annual Report.

Unlisted Public Companies

The applicability of Secretarial audit for public (unlisted) companies is subject to meeting requirements.

A public company (not listed) must undergo Secretarial Audit if it meets either of the following financial thresholds as per its latest audited financial statements:

- Paid-up share capital of ₹50 crore or more, OR

- Turnover of ₹250 crore or more

Even if only one of the thresholds is met, audit is mandatory.

Example: A public company with ₹30 crore capital but ₹270 crore turnover is required to conduct the audit.

Private Companies

The applicability of secretarial audit to private companies is also conditional and often misunderstood.

Generally, private companies are not required to conduct Secretarial Audit unless they meet specific criteria:

1. Based on Financial Thresholds:

Same as public companies:

- Paid-up capital ≥ ₹50 crore, OR

- Turnover ≥ ₹250 crore

2. Based on Borrowings:

Mandatory for any private company (or public company) with –

Outstanding loans or borrowings from banks or public financial institutions of ₹100 crore or more at any point during the financial year.

Even if the borrowings drop below ₹100 crore later, applicability is triggered if the threshold was met anytime during the year.

3. Based on Subsidiary Status:

A private company that is a subsidiary of a public company may be treated as a “deemed public company” under the Act and be subject to audit if the parent falls within the applicable thresholds.

A material unlisted Indian subsidiary of a listed company (as defined under SEBI (LODR) Regulations) is also required to undergo Secretarial Audit.

A subsidiary is considered material if its income or net worth exceeds 10% of the consolidated income/net worth of the listed entity.

Voluntary Secretarial Audit

Even when not mandatory, many private and unlisted companies opt for voluntary secretarial audits to:

- Strengthen corporate governance

- Build credibility with investors and lenders

- Prepare for IPO, private equity, or conversion into a public company

- Demonstrate regulatory discipline

Example: A growing startup seeking venture capital may undergo a voluntary Secretarial Audit to showcase governance readiness.

Scope of Secretarial Audit: Key Areas Covered

A Secretarial audit examines compliance under a wide range of laws and regulatory frameworks, including:

Companies Act, 2013 and Related Rules

This forms the core of the audit. The auditor verifies:

- Proper maintenance of statutory registers (e.g., Register of Members, Directors, Charges)

- Timely filing of forms and returns with the Registrar of Companies (ROC)

- Documentation of Board Meetings, AGMs, and Committee Meetings

- Appointment and resignation of directors and key managerial personnel (KMPs)

- Compliance with Secretarial Standards (SS-1 & SS-2) issued by ICSI

- Share capital management (issue, transfer, buy-back)

- Managerial remuneration and related party transactions

- Corporate Social Responsibility (CSR) compliance, if applicable

- Significant Beneficial Ownership (SBO) disclosures

SEBI Laws and Regulations (For Listed Companies)

For listed entities, the audit covers SEBI compliance including:

- SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015 (LODR):

- Composition of Board and Committees (Audit, Nomination & Remuneration, Stakeholders)

- Timely disclosures of material events to stock exchanges

- Related party transaction policies

- SEBI (Prohibition of Insider Trading) Regulations, 2015

- SEBI (Substantial Acquisition of Shares and Takeovers) Regulations, 2011

- SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2018

- Other relevant SEBI regulations (e.g., Buy-back, Delisting, Preferential Allotments)

Example: The PCS ensures that insider trading prevention measures, including code of conduct and trading windows, are implemented.

Foreign Exchange Management Act (FEMA), 1999

Applicable to companies involved in foreign transactions, the audit includes:

- Foreign Direct Investment (FDI) compliance

- Overseas Direct Investment (ODI)

- External Commercial Borrowings (ECBs)

- Remittances and export/import transactions

- Adherence to RBI guidelines and proper documentation of transactions

Example: The auditor will check whether FDI inflows were reported through the RBI’s FIRMS portal within the prescribed timeline.

Depositories Act, 1996 and Related Regulations

Particularly for companies with dematerialized shares, the audit covers:

- Compliance with NSDL and CDSL operational guidelines

- Timely corporate actions like dividend payments and bonus issues in demat form

- Proper reconciliation of share capital audit reports

- Safeguarding investor interests in the demat system

Industry-Specific and General Laws

Depending on the business, the audit also includes verification of:

- Labour Laws: PF, ESI, Bonus, Gratuity, etc.

- Environmental Laws: Environmental Protection Act, Water and Air Pollution Acts

- Industry-Specific Laws:

- Banking and Insurance Laws

- Telecom Regulatory Framework

- Pharma and Medical Devices Regulations

- Food Safety (FSSAI), if applicable

- Competition Act, 2002: For companies in dominant market positions

Governance and Board-Level Compliance

The scope also involves assessing the company’s governance framework:

- Constitution and Composition of the Board: Presence of independent, non-executive, and woman directors as required

- Functioning of the Board and Committees: Frequency, attendance, and quality of deliberations

- Internal Controls: Whether internal systems exist for compliance monitoring

- Disclosures and Transparency: Adequacy and timeliness of disclosures to shareholders, regulators, and stakeholders

System and Process Review

This part ensures that compliance is not incidental, but built into the operational workflow.

The Secretarial Auditor also evaluates the robustness of the company’s internal systems, including:

- Compliance monitoring mechanisms

- Delegation of authority and signing protocols

- Reporting systems for legal and regulatory updates

- Maintenance of policies and Standard Operating Procedures (SOPs)

Who Conducts Secretarial Audit: Appointment of Secretarial Auditor

Under Section 204 of the Companies Act, 2013, the Secretarial Audit of a company can only be conducted by a Company Secretary in Practice (PCS).

Internal company secretaries, chartered accountants, or cost accountants are not authorized to conduct a Secretarial Audit.

A Practicing Company Secretary is:

- A qualified member of the Institute of Company Secretaries of India (ICSI)

- Holds a valid Certificate of Practice (CoP) issued by ICSI

- Is not in full-time employment with any organization

- May practice individually or as part of a firm of Company Secretaries

For listed companies and their material unlisted subsidiaries, the Secretarial Auditor must also be peer-reviewed, i.e., hold a valid Peer Review Certificate from ICSI as per SEBI (LODR) Regulation 24A.

Appointment Process of Secretarial Auditor

The appointment of the Secretarial Auditor is a Board-driven process and follows the following steps:

- Board Meeting: The Board of Directors approves the appointment of the PCS through a formal Board Resolution in a properly convened meeting.

- Audit Committee Recommendation: If the company has an Audit Committee, the appointment must first be recommended by the Audit Committee.

- Consent & Eligibility Certificate: The PCS provides a formal letter of consent and a certificate of eligibility and independence (as per ICSI code of conduct).

- ROC Filing (Form MGT-14): Public companies are required to file the Board Resolution with the Registrar of Companies (ROC) in Form MGT-14 within 30 days of passing the resolution.

- Issue of Appointment Letter: The company issues a formal Letter of Appointment or Engagement Letter to the PCS, outlining scope, terms, and fees.

- Acceptance by PCS: The PCS acknowledges and formally accepts the engagement.

- Audit Execution: PCS conducts the audit and prepares the Secretarial Audit Report in Form MR-3, which is then annexed to the company’s Board Report.

Under the Companies Act, the Secretarial Auditor is legally liable for:

- Section 448: False statements made in any return, report, or document are punishable.

- Section 447: Fraudulent reporting is treated as fraud, punishable by imprisonment and fine.

How is It Done: Process of Secretarial Audit

The Secretarial Audit is typically conducted in four key phases:

Phase 1: Planning & Preparation

1. Appointment of Secretarial Auditor: The Board of Directors appoints a PCS by passing a Board Resolution.

The PCS provides:

- Letter of acceptance

- Consent letter

- Eligibility & independence certificate

2. Understanding the Company: PCS studies the:

- Business structure

- Legal entity setup (subsidiaries, joint ventures)

- Regulatory environment (industry-specific laws)

3. Audit Planning: PCS prepares:

- Customized Compliance Checklist (Companies Act, SEBI, FEMA, etc.)

- Audit program and timeline

A Preliminary Information Request is sent to the company.

Phase 2: Execution & Verification

4. Collection of Documents: The PCS collects and reviews a wide range of documents including:

- Incorporation documents: MoA, AoA, certificates

- Statutory registers: Members, Directors, Charges, etc.

- Meeting records: Board, Committee, AGM, EGM minutes

- Regulatory filings: MGT-7, AOC-4, DIR-12, PAS-3, etc.

- SEBI/Stock Exchange filings (for listed companies)

- Contracts and agreements: Loan agreements, related party transactions, etc.

5. Verification & Compliance Check: The PCS verifies whether the company has complied with:

| Standard | Examples |

| Companies Act, 2013 | Board meetings held on time, proper disclosures, maintenance of statutory records |

| SEBI (LODR) | Timely filings, insider trading compliance, related party transactions |

| FEMA / RBI | FDI/ODI compliance, ECB guidelines |

| Secretarial Standards | Compliance with SS-1 and SS-2 for meetings |

| Industry-specific laws | Environmental laws, labour laws, licensing requirements |

6. Discussions with Management: PCS meets with:

- Company Secretary

- CFO/Compliance Officer

- Legal Head

- Directors (if needed)

These discussions help clarify doubts and identify grey areas or hidden risks.

7. Assessment of Internal Controls: PCS evaluates:

- The adequacy of internal compliance systems

- The level of management oversight

- Record-keeping practices

- Reporting structures

Phase 3: Reporting & Finalization

8. Drafting of Audit Report: PCS prepares a draft Secretarial Audit Report (Form MR-3) which includes:

- Observations of compliance

- Qualifications or non-compliance instances

- Suggestions for improvement

- Management’s response to adverse remarks

9. Finalization of MR-3: After incorporating management inputs, PCS finalizes the MR-3 and signs it.

10. Submission to the Board: The final MR-3 report is submitted to the Board of Directors.

- It must be annexed to the Board’s Report in the company’s Annual Report.

- If any qualifications are made, the Board must explain the reasons and corrective actions in the Board’s Report.

Phase 4: Post-Audit Follow-Up

11. Board Action & Compliance Rectification: The Board is expected to:

- Discuss the audit findings

- Formulate a compliance improvement plan

- Rectify deficiencies and ensure no recurrence

12. Ongoing Monitoring & Follow-Up: In the next year’s audit, the PCS checks if past issues have been resolved. This ensures a continuous improvement cycle.

Secretarial Audit Report: Form MR-3

Form MR-3 is the prescribed format under Rule 9 of the Companies (Appointment and Remuneration of Managerial Personnel) Rules, 2014.

This report provides an independent professional opinion on the company’s compliance with:

- Corporate laws

- Secretarial Standards

- SEBI regulations (for listed entities)

- Other applicable legal frameworks

Form MR-3 Format

The form must contain:

- To Whom Addressed: “To the Members of [Company Name]”

- Introductory Paragraph:

- Mentions audit period (financial year)

- Basis of audit (books, papers, minutes, filings, etc.)

- Interaction with management and KMPs

- Scope of Audit:

- Examination of relevant records

- Review of applicable laws and Secretarial Standards

- Reliance on management declarations

- List of Laws Verified:

- Companies Act, 2013

- SEBI Laws (LODR, PIT, ICDR, SAST, etc.)

- FEMA, RBI Regulations

- Depositories Act

- Other industry-specific and general laws (labour, environment, etc.)

- Opinion of the PCS:

- Whether the company has complied with applicable laws

- Whether it maintained proper records

- Observations / Qualifications:

- Any non-compliances, deviations, or adverse remarks

- Clearly stated with reference to specific laws or regulations

- Any inability to express an opinion, if applicable

- Other Reporting Requirements (SEBI LODR, FEMA, etc.)

- Assurance on Corporate Governance:

- Company has followed good corporate practices

- There exists a compliance system within the organization

- Limitations & Disclaimers:

- Audit is based on documents and information provided

- Auditor does not express opinion on financial statements

- Professional Responsibility:

Mentions that false/misleading statements may invoke penal provisions under Sections 447 (fraud) and 448 (false statement) of the Companies Act

- Signature & Details of PCS:

Name, Membership No., COP No., Peer Review No. (if applicable), Place and Date

Contents of a Typical Secretarial Audit Report (MR-3)

| Section | Description |

| Company Details | Name, CIN, Registered Office |

| Audit Period | Financial year under review |

| Documents Reviewed | Statutory registers, minutes, filings, policies |

| Applicable Laws Examined | Companies Act, SEBI laws, FEMA, Depositories Act, etc. |

| Secretarial Standards | SS-1 and SS-2 (meetings of board and members) |

| Audit Methodology | Review of records, management discussion |

| Auditor’s Opinion | Statement on compliance status |

| Observations & Qualifications | List of non-compliances or procedural lapses |

| Recommendations | Suggestions for corrective action |

| Auditor’s Declaration | On independence and professional diligence |

| Signature Block | PCS Name, Membership, COP No., Peer Review Certificate No. |

Secretarial Audit Checklist India

Here’s a sample checklist that can be used as a reference by companies for secretarial audits.

However, the checklist should be customized based on the specific nature, size, and complexity of the company.

Benefits of Secretarial Audit

The Secretarial Audit provides a wide range of advantages beyond mere compliance.

Ensures Legal & Regulatory Compliance

Verifies adherence to multiple laws including Companies Act, 2013. SEBI Regulations (LODR, SAST, PIT, etc.), FEMA & RBI Guidelines, etc.

This minimizes exposure to penalties, notices, legal disputes, and regulatory scrutiny.

Early Detection of Non-Compliances

Helps identify gaps, irregularities, or oversights in documentation, filings, or processes.

Enables timely corrective action before issues escalate into regulatory violations or reputational harm.

Improves Corporate Governance

Reinforces accountability, integrity, and transparency in the functioning of the Board and management.

Aligns company practices with Secretarial Standards, good governance principles, and stakeholder expectations.

Enhances the effectiveness of internal compliance frameworks.

Protects Directors and Key Management

Demonstrates that directors exercised due diligence, reducing risk of personal liability under various legal provisions.

Serves as a compliance shield in regulatory investigations or shareholder disputes.

Builds Stakeholder & Investor Confidence

A clean Secretarial Audit Report (Form MR-3) sends a positive signal to:

- Investors and Shareholders

- Creditors and Banks

- Regulators and Exchanges

- Potential Joint Venture/Acquisition Partners

Enhances the company’s credibility, transparency, and investment-worthiness.

Improves Internal Controls & Efficiency

Evaluates effectiveness of internal systems, statutory registers, record-keeping, and compliance processes.

Highlights operational inefficiencies and suggests improvements.

Strategic Readiness for Business Events

Facilitates smoother:

- Mergers & Acquisitions

- Private Equity or Venture Capital Investments

- Initial Public Offerings (IPO)

- Regulatory Inspections & Due Diligence

Ensures companies are always “compliance-ready”, adding value during corporate restructuring or expansion.

Voluntary Value for Private Companies

Though not mandatory for all private companies, voluntary secretarial audits offer:

- Enhanced governance reputation

- Easier access to institutional funding

- Better preparedness for future listing