Expert verified

Expert verified In India, the role of independent directors in Statutory audit oversight is crucial. They act as gatekeepers of corporate governance, ensuring the audit process is fair and ethical.

Here’s a simple guide that breaks down their role in statutory audits and audit committees under different regulations and laws like Companies Act 2013.

What is Statutory Audit Oversight in India?

Statutory audit oversight is the framework of rules, regulators, and monitoring mechanisms.

They ensure that these audits are conducted independently, ethically, and in compliance with legal and financial standards.

Statutory audit oversight is not done by just one person or authority. It includes:

- The Audit Committee (made up of directors, including independent directors)

- The Board of Directors

- Regulatory bodies like SEBI, MCA, and sometimes ICAI

Statutory audit oversight is important as it:

- Ensures Auditor Independence: Prevents undue influence from management

- Protects Investors & Stakeholders: Provides confidence in the accuracy of financial reports

- Detects and Deters Fraud: Acts as a check on corporate misconduct (e.g., Satyam, IL&FS cases)

- Aligns with Global Standards: Strengthens India’s reputation in global financial markets

Scope of Statutory Audit Oversight in India

- Compliance Monitoring: Ensures auditors and companies follow accounting standards, auditing norms, and legal requirements (e.g., Companies Act, SEBI rules).

- Audit Quality Reviews: Reviews audit processes to assess quality, detect systemic issues, and improve professional practices.

- Fraud and Misstatement Detection: Ensures audits report red flags like fraud, poor internal controls, or financial irregularities (e.g., under CARO 2020).

- Disciplinary Actions: Regulators like NFRA, ICAI, and SEBI can penalize or debar auditors and take action against company management.

- Governance Oversight: Monitors the role of audit committees, auditor independence, appointment, and rotation practices to ensure integrity.

Who are Independent Directors?

Independent directors are non-executive board members who do not have any material, financial, or managerial ties to the company, its promoters, or management.

They provide impartial oversight, ensure ethical governance, and protect stakeholder interests (especially minority shareholders).

Key Features:

- Not part of day-to-day management

- Must not be a promoter or related to the promoters of the company

- Must not have had any material pecuniary relationship with the company in recent years

- Must have experience and integrity

- Must follow rules under the Companies Act, 2013 and SEBI Regulations

- Primarily help in audit, risk management, compensation, and governance

- Brings impartial and unbiased perspectives to Board decisions

Legal Framework Governing Independent Directors in India

Several key laws outline the rights, roles, and responsibilities of independent directors. Here’s a look at them:

1. Companies Act, 2013 (Section 149 & Rules)

This is the main law that defines and governs independent directors.

Applicability:

- Listed companies: At least 1/3 of the Board must be independent directors.

- Unlisted public companies: At least 2 independent directors if:

- Paid-up share capital ≥ ₹10 Cr

- Turnover ≥ ₹100 Cr

- Loans/debentures/deposits ≥ ₹50 Cr

Key Provisions:

- Section 149(6): Lists who can qualify as an independent director

- Section 149(10): Term of office: 5 years, renewable once; 3-year cooling-off after two terms

- Section 149(12): Liability: limited unless there’s fraud or negligence

- Schedule IV: Code of conduct for independent directors

2. SEBI (LODR) Regulations, 2015

These are rules by the Securities and Exchange Board of India for listed companies.

Important points:

- Minimum 1/3rd of the board must be independent directors

- Audit Committee must have majority independent directors

- They must meet at least once a year without other board members (exclusive meeting)

- Must review risk management, related party transactions, and auditor independence

- Removal requires dual approval: Majority of all shareholders + Majority of minority (non-promoter) shareholders

3. Oversight Bodies

- National Financial Reporting Authority (NFRA): Investigates misconduct in listed/large companies

- Institute of Chartered Accountants of India (ICAI): Regulates independent directors in smaller companies.

Ministry of Corporate Affairs (MCA) & Other Guidelines: Releases notifications, clarifications, and best practices. Also responsible for the Independent Directors’ Data Bank for training and registration

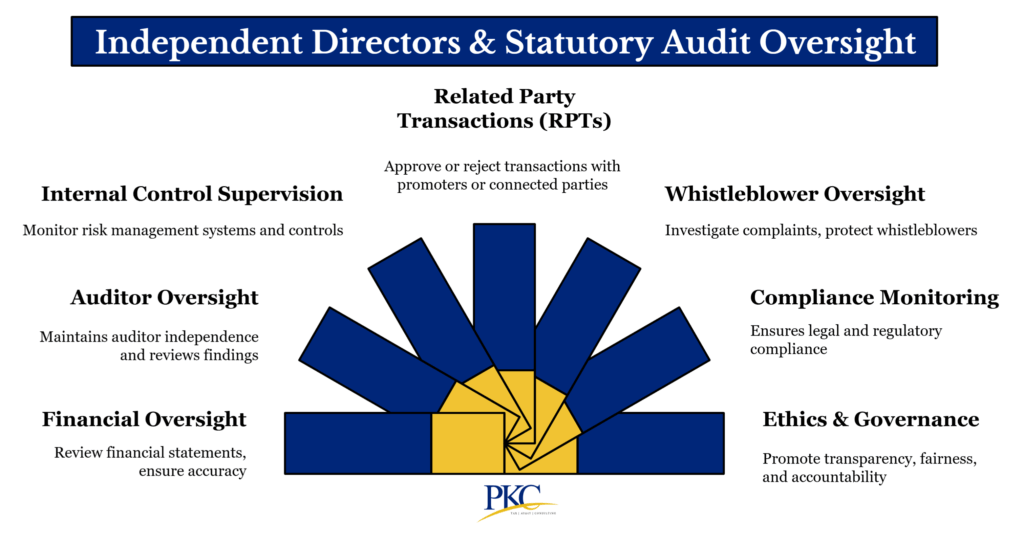

Key Roles & Responsibilities of Independent Directors in Audit Committee & Statutory Audit Oversight

Independent Directors play a critical governance role in statutory audit oversight.

Their presence in the Audit Committee ensures oversight that is free from management influence, helping to safeguard the interests of all shareholders, especially minority investors.

Here’s what they

1. Upholding Integrity in Financial Reporting

- Review Accuracy and Fairness: Verify that quarterly and annual financial statements present a true and fair view of the company’s financial health.

- Check Compliance: Ensure financial disclosures comply with Indian Accounting Standards, the Companies Act, 2013, and Schedule III requirements.

- Scrutinize Key Judgments: Assess complex accounting areas like revenue recognition, loan loss provisions, impairments, and asset valuations.

- Review Non-GAAP Measures: Ensure that any non-GAAP metrics in earnings releases are clearly reconciled and not misleading.

2. Audit Committee Leadership & Functioning

- Audit Committee Key Member: Serve as the two third of key members of the Audit Committee, as required by the Companies Act, 2013 and SEBI regulations.

- Active Participation: Participate in at least four meetings a year, focusing on financial results, audit findings, internal controls, and related party transactions (RPTs).

- Record Dissent: Clearly express and document dissenting opinions if concerns remain unresolved.

3. Appointment & Oversight of Statutory Auditors

- Select External Auditors: Recommend the appointment, reappointment, or removal of the statutory auditors.

- Ensure Auditor Independence: Assess potential conflicts of interest, pre-approve non-audit services, and monitor compliance with auditor independence norms.

- Audit Plan Review: Review audit scope, methodology, and adequacy of resources.

4. Internal Audit, Controls & Risk Management

- Internal Control Framework: Oversee the design and effectiveness of Internal Financial Controls (IFC/ICFR) using frameworks like COSO.

- Risk Mitigation: Monitor systems to detect and prevent fraud, financial misstatements, and operational risks.

- Remediation of Weaknesses: Ensure timely corrective action on control deficiencies identified by internal or external auditors.

5. Review of Audit Findings

- Discuss Audit Results: Review and discuss external and internal audit reports, key findings, and red flags.

- Ensure Follow-Through: Hold management accountable for addressing audit issues and closing gaps effectively.

- Call for Forensic Audits: Where needed, recommend special or forensic audits to investigate serious irregularities.

6. Review & Approval of Related Party Transactions (RPTs)

- Approval Authority: Approve all material RPTs as per SEBI LODR. Only they can approve transactions exceeding thresholds.

- Fairness Check: Ensure RPTs are at arm’s length, properly disclosed, and free from conflicts of interest.

- Omnibus Approval: Provide blanket approvals for recurring transactions under defined conditions.

7. Whistleblower Mechanism & Ethics Oversight

- Whistleblower Protection: Oversee the vigil mechanism and ensure employees can report concerns without fear of retaliation.

- Impartial Investigation: Independently review whistleblower complaints, especially those related to fraud, mismanagement, or financial misconduct.

- Promote Ethical Conduct: Uphold the Code of Conduct, encourage ethical behavior, and support a culture of transparency.

8. Legal & Regulatory Compliance

- Statutory Compliance: Ensure adherence to the Companies Act, 2013, SEBI (LODR) Regulations, 2015, and other applicable laws.

- Disclosure Requirements: Oversee timely and accurate regulatory filings, including annual reports, proxy statements, and audit committee disclosures.

9. Stakeholder Protection & Governance

- Protect Minority Shareholders: Act as guardians of stakeholder rights, ensuring fair and unbiased decisions by the board and management.

- Promote Good Governance: Encourage best practices in audit oversight, risk management, and board functioning.

- Build Investor Confidence: Reinforce trust in the company through transparent reporting and strong ethical oversight.

10. Performance Evaluation

- Self & Board Assessment: Participate in regular evaluations of the board, Audit Committee, executive management, and their own role as independent directors.

- Continuous Improvement: Use performance feedback to strengthen governance frameworks and improve audit oversight quality.

11. Reviewing and Assessing Audit Quality

- Audit Quality Reviews: Participate in audit quality reviews and ensure that the audit process reinforces good governance and detects material errors, irregularities, or instances of fraud.

- Recommend Improvements: In auditing practices, controls, and disclosures.

Frequently Asked Questions

1. What is the role of independent directors in statutory audit oversight?

Independent directors monitor the audit process to ensure financial transparency and regulatory compliance. They help detect fraud, review auditor reports, and enforce ethical reporting standards.

2. How do independent directors ensure auditor independence?

They help appoint statutory auditors and review their relationships with the company. They also ensure auditors follow ethical guidelines and don’t have conflicts of interest.

3. Can independent directors be held liable for audit failures?

Yes, but only if they are directly involved in fraud or if they neglect their duties. They are generally protected if they act honestly and in good faith.

4. What is the difference between internal and statutory audit oversight?

Internal audit oversight focuses on daily operations and controls, often handled by employees. Statutory audit oversight involves external audits reviewed by the audit committee and independent directors.

5. Can an independent director serve on multiple audit committees?

Yes, but there are limits. They must be able to give enough time and attention to each company, as per SEBI and MCA guidelines.