Expert verified

Expert verified Sending money abroad as an NRI can be complicated owing to the regulations and rules that need to be followed. Knowing the basics of NRI repatriation of funds from India can help.

Understand with us repatriation essentials for NRIs. We cover everything from repatriation limits for NRIs, to the process, tax and documentation requirements and more.

What is Repatriation of Funds for NRIs?

Repatriation of funds refers to the legal and regulated process through which Non-Resident Indians (NRIs) transfer money from their Indian bank accounts to bank accounts in their country of residence.

This involves converting Indian Rupees (INR) into a foreign currency (e.g., USD, GBP, EUR) and ensuring compliance with Indian rules and regulations.

Repatriation is different from standard money transfer as it involves tax clearances, regulatory documentation, and account-specific rules.

Common Use Cases for Repatriation

NRIs repatriate funds for various personal and financial reasons, including:

- Managing global cash flow and personal finances.

- Investing in international markets or property.

- Funding education, medical expenses, or family support abroad

- Repatriating proceeds from sale or inheritance of Indian property

- Returning home and transferring savings back.

Key Regulations for NRI Repatriation

Repatriation of funds for NRIs is a regulated process and must comply with Indian laws to ensure legitimacy, tax compliance, and adherence to exchange control norms.

Here’s a breakdown of the key legal, financial, and procedural aspects of NRI repatriation under Indian law:

1. FEMA: The Core Framework for Repatriation

The Foreign Exchange Management Act (FEMA), is the primary law that governs foreign exchange transactions in India.

All repatriations made by NRIs are subjected to the provisions laid down by FEMA. It ensures that any funds being repatriated abroad are sourced from legitimate channels, making sure the transaction is fully compliant with Indian laws.

2. RBI Guidelines on Repatriation

The Reserve Bank of India (RBI) oversees the repatriation process. Key regulations provided by the RBI include:

- Eligible Individuals: Only NRIs (Non-Resident Indians) and PIOs (Persons of Indian Origin) with eligible accounts are allowed to repatriate funds.

- Annual Limits: Establishes annual limits for repatriation, especially from Non-Resident Ordinary (NRO) accounts, with a cap of USD 1 million per financial year.

- Required Documentation: Prescribes certain forms and documents, which must be submitted to facilitate the repatriation of funds.

3. Indian Income Tax Act

The Indian Income Tax Act, 1961 also plays a critical role in regulating the taxation of income earned by NRIs and repatriated abroad. It provides provisions for:

- Tax on NRO Account Income:

- Capital Gains Tax

- DTAA Benefits

Governing Laws & Regulatory Authorities:

| Authority | Role |

| FEMA (1999) | Governs all foreign exchange transactions including remittances and repatriation |

| RBI | Issues guidelines and directions for operational compliance |

| Income Tax Act (1961) | Governs taxation on income being repatriated |

Types of NRI Bank Accounts and Repatriation Rules

Repatriation rules vary significantly depending on the type of NRI bank account held in India. Here’s what you need to know:

1. Non-Resident External (NRE) Account

It is used to park foreign income (e.g., salary, business earnings) in India. It is ideal for NRIs looking to freely move foreign income back abroad.

- Fully repatriable: Both principal and interest can be transferred abroad without limits

- Taxation: Interest earned on NRE accounts is tax-free in India.

Key Rules:

- Only foreign income can be credited.

- Funds can be transferred freely to any country, without restrictions.

- Joint account holders can include resident Indians (close relatives).

- Usually requires a FEMA declaration form (Form A2) for remittances.

2. Non-Resident Ordinary (NRO) Account

Used to manage income earned in India (e.g., rent, dividends, pensions, property sale proceeds).

- Repatriation: Limited repatriability, Capped at USD 1 million per financial year (April-March), including principal and interest

- Taxation: Interest earned is taxable in India. TDS applies, and the tax rate depends on the type of income.

Key Rules:

- Repatriation is subject to tax clearance.

- Requires Form 15CA (self-declaration) and Form 15CB (Chartered Accountant certificate) to prove tax compliance.

- Repatriation limits apply to capital income (e.g., property sale proceeds), but current income (e.g., rent, dividends) can be repatriated without limits, subject to tax and documentation.

- Requires tax certificates and proof of income source for repatriation.

3. Foreign Currency Non-Resident (FCNR) Account

Meant for NRI term deposits held in foreign currencies like USD, GBP, EUR, etc.

- Repatriation: Fully repatriable. Both principal and interest can be transferred freely, with no restrictions on the amount.

- Taxation: Interest earned on FCNR accounts is tax-free in India.

Key Rules:

- Deposits are in foreign currency, protecting against currency fluctuations.

- No currency conversion is required during repatriation.

- Requires Form A2 (FEMA declaration) to initiate the transfer.

Tax Compliance & Documentation Requirements for NRI Repatriation

Repatriating funds from India as an NRI can indeed be a complex process due to the various tax and regulatory requirements involved.

Here’s a look at the tax compliance and documentation necessary for smooth repatriation:

Tax Compliance for Repatriation

Before transferring funds from India to your overseas account, it’s essential to ensure that all taxes related to the funds being repatriated have been duly paid.

Follow these key steps you must take to remain compliant:

Identify the Source of Funds

- Rental Income: Subject to TDS at 30% + surcharge + cess.

- Capital Gains (Property Sales):

- Short-Term Capital Gains (STCG): 30% TDS.

- Long-Term Capital Gains (LTCG): 20% TDS with indexation (if the asset is held for more than 2 years).

- Interest on NRO Account: TDS at 30%.

- Interest on NRE/FCNR Accounts: Tax-free in India.

TDS Deduction

Banks or the buyer (in case of property sales) will deduct the applicable TDS before funds are disbursed to you.

If your actual tax liability is lower than the deducted TDS rate, you can apply for a Lower Deduction Certificate from the Income Tax Department.

Double Taxation Avoidance Agreement (DTAA)

If your country of residence has a DTAA with India, you may be eligible for reduced tax rates on repatriated funds.

You can use the tax paid in India to claim a credit for taxes paid in your home country, avoiding double taxation.

Required Documentation for Repatriation

There are several documents you must submit to both your bank and tax authorities to ensure compliance. Here’s a detailed breakdown:

Mandatory Forms

- Form 15CA (Self-declaration):

- Filed online on the Income Tax Department portal.

- States the nature of the payment and confirms that the applicable taxes have been paid.

- Required for: All remittances that exceed ₹5 lakh or are taxable in India.

- Form 15CB (Chartered Accountant’s Certificate):

- Issued by a CA, confirming that taxes have been deducted or paid.

- Required for most remittances above ₹5 lakh or taxable in India.

- Form A2 (FEMA Declaration): Declaration for all outward remittances, as required by FEMA. This ensures that the funds are being repatriated for a legitimate purpose.

Supporting Documentation

- NRI’s Identity Verification:

- Copy of Passport (including visa/residency permit),

- Copy of PAN Card (mandatory for tax tracking),

- Proof of Overseas Address (such as utility bills or bank statements).

- Proof of Source of Funds: Depending on the origin of the funds:

- For Rent: Lease or rental agreement and TDS certificates (Form 16A).

- For Dividends/Interest: Dividend statements, TDS certificates.

- For Sale of Assets: Sale deeds, proof of original investment, capital gains tax calculation.

- For Inherited Funds: Death certificate, will or legal heir certificate, probate (if applicable).

- Tax Payment Proof: Challans or receipts confirming that taxes (like capital gains tax) have been paid.

- Repatriation Request Form: The bank-specific form to initiate the transfer.

- Proof of Property Ownership (for property sales): Title deeds or sale agreements.

Banks usually assist with this documentation, but consulting a NRI specialist from firms like PKC Management Consulting is highly recommended to avoid delays or compliance issues.

Special Considerations

- Inheritance: When repatriating funds from inherited assets, ensure you have the necessary documents like the death certificate, will, legal heir certificate, and tax clearance for the inherited funds.

- Capital Gains Tax: For property sales, it’s important to ensure that the TDS has been deducted correctly and that you have a certificate of TDS (Form 16B) issued by the buyer.

- Rental Income: Ensure you have TDS certificates for every year the rent was earned, and provide the lease/rental agreement as evidence.

NRI Repatriation Limits and Special Cases

RBI, Annual Repatriation Limit:

NRIs can repatriate up to USD 1 million per financial year from their NRO account. However, funds from NRE and FCNR accounts can be repatriated freely without any limit.

Property Sale Proceeds:

- Proceeds from the sale of residential or commercial properties can be repatriated, but only up to the amount initially invested (which must be sourced from NRE or FCNR accounts).

- Agricultural land, plantation properties, or farmhouses cannot be repatriated, and any sale proceeds must remain within India.

- Inheritance: If the funds being repatriated are from an inheritance, these can be repatriated up to the USD 1 million cap per year, provided the necessary documentation is submitted.

Special Permissions for Exceeding Limits

In cases where the repatriation exceeds the USD 1 million limit, NRIs can apply to the RBI for special permission. This may be granted under specific circumstances such as:

- Medical Expenses

- Educational Expenses

- Home Purchase

Residency Status and Impact on Repatriation

If an NRI returns to India permanently, they must convert their NRO/NRE accounts into resident accounts as per the RBI Master Circular.

This can create temporary challenges in repatriation, especially if funds are held in accounts

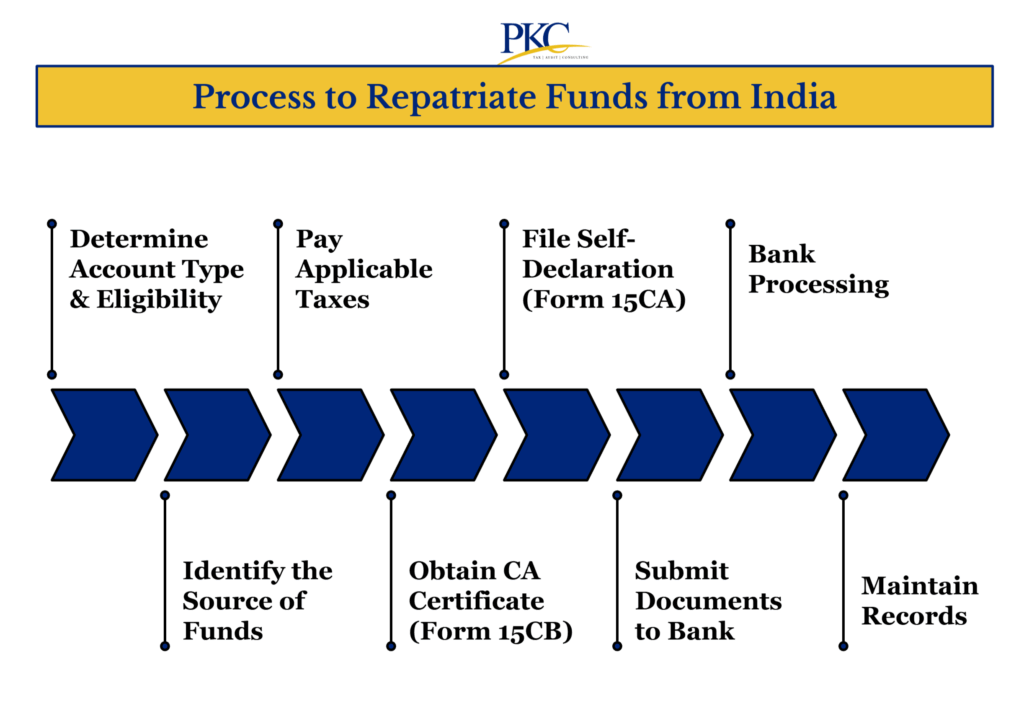

Step-by-Step Process to Repatriate Funds from India

Here’s a simple breakdown of how you can repatriate funds as an NRI:

1: Determine Account Type & Eligibility

- NRE / FCNR accounts allow unlimited repatriation of both principal and interest.

- NRO accounts allow repatriation up to USD 1 million per financial year, after taxes and proper documentation.

2: Identify the Source of Funds

Understand where the money came from:

- Rental income: Subject to 30% TDS.

- Interest on NRO deposits:TDS at 30%.

- Sale of property: Capital Gains Tax applies (short or long-term).

- Inherited assets: Ensure the deceased’s taxes are cleared.

- Dividends: Usually exempt, but verify current tax rules.

3: Pay Applicable Taxes

- Confirm TDS is correctly deducted (e.g., Form 16A for rent, 16B for property sales).

- If excess TDS was deducted, consider applying for a Lower/Nil TDS Certificate.

- Calculate and pay capital gains tax using indexation if applicable.

- File income tax returns (if needed) and keep tax receipts/challans as proof.

4: Obtain CA Certificate (Form 15CB)

- Hire a CA

- Provide documents like sale deeds, rent agreements, bank statements, and tax receipts.

- The CA verifies transactions, calculates taxes, and submits Form 15CB online using a digital signature.

5: File Self-Declaration (Form 15CA)

- Log in to the Income Tax portal using your PAN.

- Submit Form 15CA online under the correct section (Part A for < ₹5 lakh, Part C for > ₹5 lakh with 15CB).

- Download and print the acknowledgment.

6: Submit Documents to Bank

Provide your bank with:

- Forms 15CA & 15CB

- Form A2 (remittance declaration)

- PAN card, passport, visa/OCI/PIO

- Proof of overseas address, income source, and tax payments

- NRO account statement

7: Bank Processing

The bank reviews all documents for tax and FEMA compliance, then converts funds to foreign currency.

It then transfers them to your overseas account. Make sure the USD 1 million cap isn’t exceeded.

8: Maintain Records

Keep all forms, certificates, challans, and proofs for 8 years, in case of a future audit.

FAQs On Tax on Repatriation of Funds from India for NRIs

1. What is the repatriation tax in India?

Repatriation tax in India refers to the income tax and TDS that must be paid on funds earned in India before sending them abroad. The rate depends on the source of funds.

2. How much money can you repatriate from India?

NRIs can repatriate up to USD 1 million per financial year from an NRO account after paying taxes. NRE and FCNR accounts have no repatriation limit.

3. How much tax to send money abroad from India?

The tax rate depends on the nature of income. It is typically 20% for long-term capital gains and 30% for rental or short-term capital gains. Interest on NRO accounts is also taxed at 30%, while NRE and FCNR interest is tax-free.

4. How can NRIs repatriate money from India?

NRIs can repatriate funds by ensuring taxes are paid, filing Form 15CA online, obtaining Form 15CB from a Chartered Accountant, and requesting remittance through their bank. The bank then processes the transfer under RBI and FEMA rules.

5. Which type of NRI account allows free repatriation of funds outside India without any limits?

NRE and FCNR accounts allow unlimited repatriation of both principal and interest. NRO accounts are subject to a USD 1 million per year limit and tax compliance.