Expert verified

Expert verified Compliance for Indian subsidiary of foreign companies include adhering to a wide array of legal and regulatory requirements.

This guide will break down each compliance requirement for subsidiaries. These include FEMA, RBI, MCA, tax and labour compliance requirements.

You can also download a FREE foreign subsidiary compliance checklist at the end.

What is a Subsidiary of a Foreign Company in India?

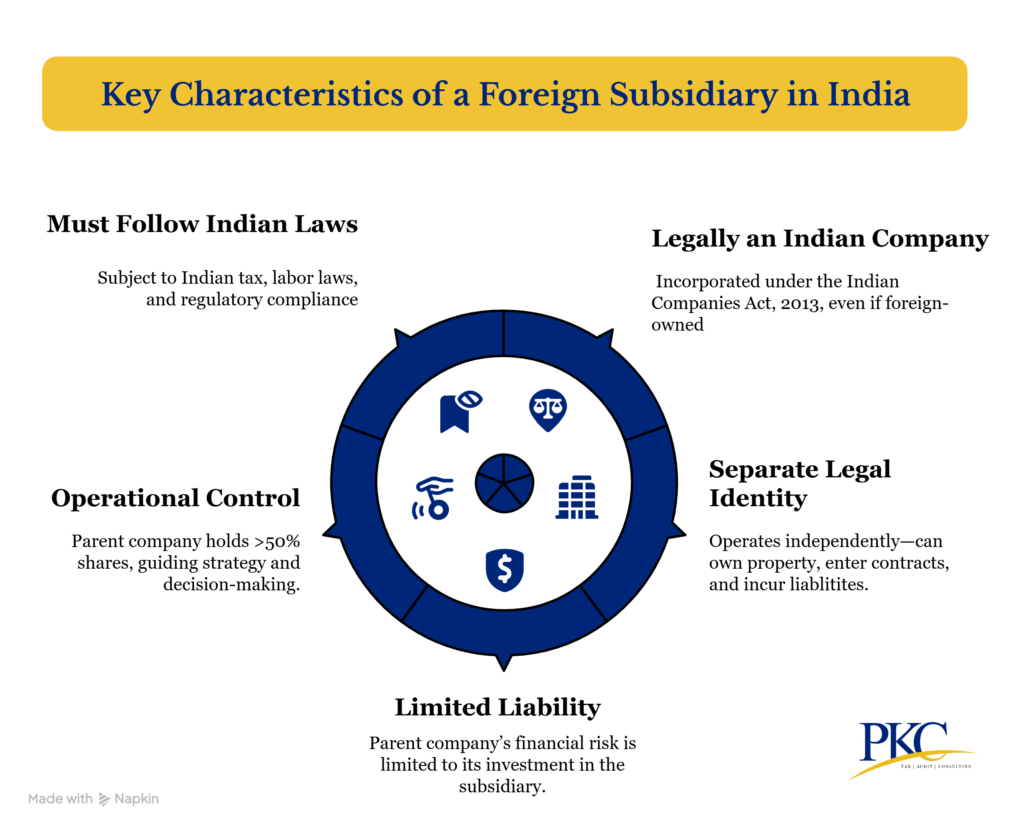

A subsidiary of a foreign company in India refers to an Indian company that is either fully or partially controlled by a foreign parent company.

The foreign – “parent” or “holding” – company, holds a significant portion (usually more than 50%) of the shares in the Indian subsidiary, which gives it control over the subsidiary’s management and operations.

Types of Foreign Subsidiaries in India

Foreign subsidiaries in India can be categorized based on the ownership structure of the parent company as:

1. Wholly Owned Subsidiary (WOS)

Foreign parent company owns 100% of the shares in the Indian subsidiary and has full control over its operations, management, and financial matters.

This allows the foreign company to safeguard its proprietary technology, maintain complete operational control, and avoid conflicts with local partners.

- Complete Control: Parent company enjoys full decision-making authority without the need for consensus or negotiation with Indian partners.

- Sectors with 100% FDI Allowed: Only possible in sectors where 100% FDI is allowed under Indian regulations.

2. Joint Venture / Partly Owned Subsidiary

The foreign parent company owns more than 50% but less than 100% of the shares.

The remaining shares are held by Indian entities or individual investors.

- Shared Control: The foreign parent retains control over the strategic direction, but key decisions may require collaboration with Indian partners.

- Common in Joint Ventures: Widely used in sectors such as manufacturing, retail, and telecommunications, where foreign entities collaborate with Indian partners to meet regulatory requirements or to benefit from local expertise.

Types of Compliance for Indian Subsidiary of Foreign Company

When a foreign company establishes a subsidiary in India, it is subject to a comprehensive set of legal, financial, and operational compliances.

These are the key compliance areas for an Indian subsidiary of a foreign company:

- Incorporation & Initial Compliance Requirements: Steps a foreign company must take to legally set up a subsidiary in India and to start operations.

- Company Law Compliances: Ongoing obligations under the Companies Act. Includes filing annual reports, holding regular meetings, etc.

- Corporate Governance & Secretariat Compliances: Ensures transparency in decision-making and management within the company.

- Audit & Accounting Compliance: Subsidiaries must maintain proper financial records, conduct annual audits by a certified CA, and file annual financial statements with the MCA.

- FEMA & RBI Compliances: Since the subsidiary involves foreign investment, it must comply with the FEMA and regulations from the RBI.

- Labour Law & Employment Compliance: Following labour laws to protect employee rights. Includes registration and contributions to employee welfare funds.

- Transfer Pricing & Tax Compliances: Tax regulations applicable to the subsidiary and those governing transactions between the subsidiary and its foreign parent company.

- Sector-Specific Compliances: Certain industries like finance, pharmaceuticals, have additional compliance requirements due to their nature.

Mandatory Registrations & Incorporation of Subsidiary of Foreign Company

The incorporation and initial compliance requirements for an Indian subsidiary of a foreign company include:

Business Structure & Name

Most foreign companies prefer to register their subsidiary as a Private Limited Company because it offers:

- Limited liability protection

- Full ownership control

- Easy scalability

- 100% FDI allowed in many sectors

Subsidiary name must be:

- Unique and compliant with MCA naming guidelines

- Often includes foreign parent brand followed by “India Private Limited”

Digital Signature Certificate (DSC) and Director Identification Number (DIN)

Before filing for incorporation:

- All proposed directors must acquire a Class 3 DSC to sign electronic documents on MCA portal.

- Get DIN through the MCA system. Foreign nationals must provide notarized and apostilled identity and address proofs (typically a passport).

Preparation and Filing of Incorporation Documents

Use RUN (Reserve Unique Name) service or SPICe+ form on the MCA portal to apply for:

- Name approval

- Incorporation

- PAN, TAN, GST (optional), EPFO, ESIC

Submit:

- Memorandum of Association (MoA) and Articles of Association (AoA)

- Director/shareholder IDs

- Registered office proof

- Board resolution from foreign parent

- Apostilled foreign documents

- CA/CS/lawyer declaration confirming compliance with incorporation norms

Certificate of Incorporation (COI)

Post scrutiny, the Registrar of Companies (ROC) issues the COI, which includes:

- Corporate Identification Number (CIN)

- PAN and TAN (automatically generated through SPICe+)

Now, the subsidiary becomes a separate legal entity.

Initial Compliance After Incorporation

- Open a bank account in the company’s name.

- Deposit share capital from the foreign parent company as per FDI rules.

- File INC-20A (Declaration of Commencement of Business) with MCA within 180 days of incorporation.

- Report the foreign investment to RBI by filing Form FC-GPR.

- Issue share certificates to all subscribers within 60 days of incorporation

- Display compliance registration at the registered office

Foreign Subsidiary Company Law Compliances in India

An Indian subsidiary requires strict adherence to ongoing legal and procedural compliances under the Companies Act, 2013, enforced by the MCA and ROC:

Board Meetings

- First Board Meeting must be held within 30 days of incorporation.

- A minimum of four Board Meetings must be held every financial year, with no more than 120 days between two consecutive meetings.

- Detailed notice, agenda, and minutes must be maintained as part of statutory records.

Annual General Meeting (AGM)

- First AGM must be held within 9 months from the end of the first financial year.

- Thereafter, an AGM must be conducted each year within 6 months from the end of the financial year (but not exceeding 15 months from the previous AGM).

- Key business includes:

- Adoption of financial statements

- Appointment or reappointment of auditors

- Declaration of dividends

Filing of Annual Return (Form MGT-7)

- Must file Form MGT-7 with the ROC annually.

- Includes:

- Shareholding pattern

- List of directors and KMP

- Changes in company structure

Due Date: Within 60 days of the AGM

Filing of Financial Statements (Form AOC-4)

Audited financial statements must be filed using Form AOC-4, including:

- Balance Sheet

- Profit and Loss Statement

- Directors’ Report

- Auditor’s Report

Due Date: Within 30 days of the AGM

Appointment of Auditors (Form ADT-1)

- First statutory auditor must be appointed by the Board within 30 days of incorporation.

- Subsequent appointment of auditors is for a 5-year term, filed using Form ADT-1.

Director’s KYC and Disclosures (DIR-3 KYC, DIR-8, MBP-1)

- All directors must complete DIR-3 KYC annually.

- Directors must disclose their interest in other companies/entities via Form MBP-1.

- Must confirm they are not disqualified using Form DIR-8.

Financial Audit and Board’s Report

- Company must prepare financial statements in accordance with Indian Accounting Standards (Ind AS).

- Must be audited by a Chartered Accountant.

- A Board’s Report summarizing financial performance, risk management, RPTs, and CSR (if applicable) must accompany the financial statements.

Maintenance of Registered Office

- Physical registered office must be maintained in India

- Any change must be reported using Form INC-22

- Address must be displayed on all company communication, signboards, and letterheads

Foreign Company Specific Compliances

- Form FC-1: Filed within 30 days of incorporation of the subsidiary, containing details of the foreign parent and its representatives.

- Filing of FC-GPR: Reporting FDI to the RBI within 30 days of share allotment.

- FLA Return: Filed annually by July 15 if the company has received foreign investment or made overseas investments.

Corporate Governance & Secretariat Compliances

These mechanisms ensure that the subsidiary functions in a lawful and accountable manner.

They are meant to safeguard the interests of shareholders, employees, and regulators. They cover:

Board Constitution & Independence

- Minimum of two directors, with at least one Indian resident director residing in India ≥182 days in the previous calendar year

- If the subsidiary crosses specific thresholds (e.g., net worth, turnover, profit), it must constitute:

- Audit Committee

- Nomination & Remuneration Committee

- Corporate Social Responsibility (CSR) Committee

- Independent directors are required on certain committees based on financial criteria.

Board Resolutions & Approvals

Key decisions must be approved via Board Resolutions and recorded in statutory registers. These include:

- Appointment or resignation of directors,

- Issue or allotment of shares,

- Opening of bank accounts,

- Approval of financial statements,

Director Disclosures

Every director must annually submit:

- Form MBP-1: Disclosure of interest in other entities.

- Form DIR-8: Declaration of non-disqualification.

These disclosures enhance transparency and reduce conflict of interest.

Adherence to Secretarial Standards (SS-1 & SS-2)

Issued by the Institute of Company Secretaries of India (ICSI):

- SS-1: Governs Board Meetings.

- SS-2: Governs General Meetings.

Compliance is mandatory for all companies except One Person Companies (OPCs).

Maintenance of Statutory Registers

The following must be maintained and kept updated at the registered office:

| Register | Purpose |

| Register of Members | Shareholding structure |

| Register of Directors & KMP | Key personnel details |

| Register of Charges | Loans and securities |

| Register of Loans & Investments | Loans, investments, guarantees, and securities |

| Register of Related Party Contracts | Transactions disclosure |

These must be regularly updated and available for inspection by regulators and shareholders.

Minutes of Meetings

- Accurate minutes of all Board and General Meetings must be recorded

- Must be signed by the Chairman and maintained permanently

- Legally admissible as proof of decisions taken

Filing of Resolutions and Returns with MCA

- Form MGT-14: Certain board and shareholder resolutions.

- Form MGT-7/MGT-7A: Annual Return (within 60 days of AGM).

- Form AOC-4: Financial statements (within 30 days of AGM).

- Form ADT-1: Auditor appointment (within 15 days of AGM).

- Event-based forms like DIR-12 (director changes), INC-22 (address change), PAS-3 (share allotment).

Secretarial Audit (Form MR-3)

Applicable to public companies that meet:

- Paid-up capital ≥ ₹50 crore, or

- Turnover ≥ ₹250 crore.

Must be conducted by a Practicing Company Secretary and annexed to the Board’s Report.

Event-Based Compliances (As and When Occurs)

Certain corporate actions must be reported to the ROC within specified timelines:

| Event | Form | Due Date |

| Change in directors or KMP | DIR-12 | Within 30 days |

| Allotment of shares | PAS-3 | Within 15 days |

| Increase in authorized capital | SH-7 | Within 30 days |

| Change in registered office | INC-22 | Within 15 days |

| Creation/modification of charge | CHG-1 | Within 30 days |

| Resolutions passed at board/shareholder meetings | MGT-14 | Within 30 days (for certain resolutions) |

Audit & Accounting Compliances for Indian Subsidiaries

Indian subsidiaries of foreign companies must meet stringent audit and accounting compliance standards. These are governed by:

- Companies Act, 2013

- Income Tax Act, 1961

- Indian Accounting Standards (Ind AS)

- Rules issued by the Institute of Chartered Accountants of India (ICAI)

Maintenance of Books of Accounts

Must maintain accurate and complete books at its registered office including.

- Cash and bank transactions

- Purchase/sales ledgers

- Fixed asset registers

- Debtors/creditors list

- Expense and payroll details

These must follow:

- Accrual system of accounting

- Double-entry bookkeeping

- Ind-AS, where applicable

Statutory Audit (Mandatory)

Provides an independent, true, and fair view of the company’s financial statements.

| Item | Details |

| Conducted By | A practicing Chartered Accountant (CA) or CA firm |

| Appointment | Appointed by the Board or Shareholders and filed with MCA via ADT-1 |

| Audit Report | Must be attached with financials and filed with ROC |

| Deadline | Complete before AGM; file AOC-4 within 30 days of AGM |

Filing of Financial Statements (Form AOC-4)

Includes:

- Balance Sheet

- Profit & Loss Account

- Cash Flow Statement

- Statement of Changes in Equity (for Ind AS)

- Notes to Accounts

- Director’s Report

- Auditor’s Report

Timeline: File within 30 days of AGM (typically by October 30 for FY ending March 31)

Annual Return (Form MGT-7)

Must be filed detailing:

- Shareholding structure

- Board of Directors and Key Managerial Personnel

- Share transfers

- Changes in directorships

Timeline: File within 60 days of the AGM

Tax Audit (Section 44AB, Income Tax Act)

For subsidiaries, with turnover > ₹10 crore, unless cash transactions are less than 5%

Filing:

- Report in Form 3CA/3CB and 3CD

- Filed electronically by September 30 of the assessment year

Transfer Pricing Audit (Form 3CEB)

Applicable if subsidiary has international or specified domestic transactions with:

- Its foreign parent

- Sister concerns

- Other related parties

Filing Requirements:

| Item | Details |

| Audit Form | Form 3CEB |

| Auditor | Independent Chartered Accountant |

| Documentation | Transfer Pricing Study Report |

| Deadline | Nov 30 of the assessment year |

Other Accounting Compliances

Withholding Tax (TDS):

- Payments to the foreign parent (e.g., royalty, technical fees) are subject to TDS under Indian law.

- Rates may be reduced under DTAA (Double Tax Avoidance Agreement) with the parent’s country.

- Must be deducted, deposited monthly, and reported via Form 15CA/15CB.

Authentication & Translation:

Documents filed with the Registrar of Companies (ROC) must be:

- Certified by a practicing professional

- Translated into English, if applicable

FEMA & RBI Compliance for Indian Subsidiary of Foreign Company

FEMA governs how foreign capital flows into and out of India.

The RBI administers these flows and ensures companies comply through timely disclosures, pricing norms, sectoral limits, and repatriation rules.

Indian subsidiaries of foreign companies can obtain investment via two routes:

- Automatic: No approval needed; covers most sectors.

- Government: Approval needed for sensitive areas like Defence, Media, Telecom.

Most tech, consulting, IT, e-commerce, and manufacturing subsidiaries operate under the Automatic Route.

Advance Reporting Form (ARF)

When an Indian subsidiary receives foreign investment from its parent company, it must report the transaction to RBI.

This is done by filing the Advance Reporting Form (ARF) on the RBI’s FIRMS (Foreign Investment Reporting and Management System) portal within 30 days of receiving the funds.

Required documents include investor’s KYC (via the Authorized Dealer bank), FIRC, Board resolution, and a CA’s certificate confirming receipt.

Allotment of Shares – Filing of Form FC-GPR

Once shares are allotted to foreign investors, the subsidiary is required to file Form FC-GPR (Foreign Currency – Gross Provisional Return) within 30 days of allotment.

This form is also filed on the FIRMS portal alongwith:

- CA’s valuation certificate

- Compliance certificate from Company Secretary

- Board resolutions

- Share subscription agreement.

Transfer of Shares – Filing of Form FC-TRS

For transfer of shares between a resident and a non-resident (or vice versa), company must file Form FC-TRS on FIRMS portal within 60 days of transfer.

This applies to both sale and purchase of shares by foreign investors.

It must comply with RBI’s pricing guidelines, ensuring the ransaction is made at fair market value certified by a CA.

Entity Master and Single Master Form (SMF)

Before filing any foreign investment-related forms, subsidiary must register itself on the FIRMS portal by submitting the Entity Master Form.

It’s a one-time registration that creates the company’s profile in RBI’s records and must be updated whenever there is any change in structure or foreign holding.

Annual Return on Foreign Liabilities and Assets (FLA Return)

Annually, the Indian subsidiary must file the FLA Return with the RBI by July 15.

It provides data on foreign investments received, liabilities to non-residents, and any overseas investments made.

This return must be filed online on RBI’s FLAIR portal and is applicable even if the subsidiary received foreign investment in previous years and not in the current year.

External Commercial Borrowings (ECB) Compliance (If Applicable)

If Indian subsidiary borrows funds from its foreign parent company or any other non-resident, it must comply with the ECB guidelines issued by RBI.

The company must first obtain a Loan Registration Number (LRN) from RBI and file ECB-2 returns monthly to report the status of the loan.

ECBs are generally permitted under Automatic Route for certain eligible borrowers and sectors, subject to end-use restrictions and compliance with interest rate and maturity norms.

Repatriation of Profits, Dividends, or Royalties

Indian subsidiaries can remit dividends, profits, or royalties to their foreign parent companies.

No RBI approval is required for such remittances under the automatic route, but the Authorized Dealer bank will require supporting documentation.

| Type | Key Compliance Requirements |

| Dividends | Freely repatriable after TDS; No RBI approval needed |

| Royalty/Fees | Allowed under specific caps; subject to withholding tax |

| Capital Gains/Sale Proceeds | Allowed with proper tax clearance, CA certificate, and bank documents |

| Bank Documents Needed | CA Certificate (Form 15CB), Undertaking (Form 15CA), Board Resolution, Tax challans, audited financials |

Downstream Investment Compliance (If Applicable)

If Indian subsidiary invests in another Indian company, it becomes a downstream investment (indirect foreign investment). Compliance includes:

- Ensuring downstream company follows sectoral caps

- Filing with RBI and DPIIT (Department for Promotion of Industry and Internal Trade)

- Obtaining board approval and making relevant disclosures

KYC and AML Requirements

RBI requires KYC verification for all foreign investors through Authorized Dealer (AD) banks

Comply with Anti-Money Laundering (AML) guidelines

Shares must be issued/transferred at or above RBI-prescribed fair valuation (determined by CA)

Tax Compliance for Indian Subsidiary of Foreign Company

An Indian subsidiary of a foreign company is a separate domestic legal entity and follows local tax laws.

Due to foreign ownership and cross-border dealings, it must however, also comply with transfer pricing rules, withholding tax, and DTAA provisions.

Corporate Income Tax

An Indian subsidiary is treated as a domestic company and taxed on its global income earned in India.

- Standard rates: 25% (if turnover ≤ ₹400 crore) or 30% (if above), plus surcharge and cess.

- Optional lower rates: 22% or 15% under Sections 115BAA/115BAB, if certain conditions are met.

- May opt for concessional tax regimes such as 22% or 15% under Section 115BAA/115BAB of the Income Tax Act, subject to conditions.

Minimum Alternate Tax (MAT)

If the company claims significant deductions and reports low taxable income, MAT ensures minimum tax is paid.

- Charged at 15% of book profits plus surcharge and cess.

- Companies opting for the concessional tax regime are exempt from MAT.

Advance Tax Payments

The subsidiary must pay taxes in advance quarterly, based on projected annual income.

- Payments are due quarterly: 15% (June 15), 45% (Sept 15), 75% (Dec 15), 100% (Mar 15).

- Interest penalties apply for underpayment or non-payment

Filing of Income Tax Return (ITR)

All Indian companies, including foreign subsidiaries, must file ITR annually using Form ITR-6.

- Deadline: October 31, or November 30 if a transfer pricing audit is required.

- Filing must include audited financials, tax audit reports, and transfer pricing documentation (if applicable)

Tax Audit under Section 44AB

If annual turnover exceeds ₹1 crore (business) or ₹50 lakh (professionals), a tax audit is mandatory.

- Conducted by a CA

- Forms: 3CA/3CB and 3CD filed electronically

- Deadline: September 30 of the assessment year.

Transfer Pricing Compliance

Cross-border dealings with related parties such as parent company must follow arm’s length pricing rules.

- Detailed documentation is required.

- Form 3CEB (Accountant’s Report) due by November 30.

- Applies to intercompany services, royalties, loans, etc.

Tax Deducted at Source (TDS)

The subsidiary must deduct TDS on specified payments (e.g., salaries, rent, contractor payments, professional fees, etc.)

- Deposit by 7th of the next month.

- Quarterly TDS returns: Form 24Q (salaries), 26Q (others).

- Issue Form 16/16A to payees.

Withholding Tax on Repatriation to Parent Company

Payments to the foreign parent (e.g., dividends, royalties) are subject to withholding tax.

- Standard rates: 10% (dividends, royalties), 20% (interest), unless reduced under DTAA.

- To claim DTAA relief: submit TRC, Form 10F, and PE declaration.

Goods and Services Tax (GST)

Registration is required if turnover exceeds ₹20–40 lakh (state-dependent).

Key filings:

- GSTR-1 (outward supplies)

- GSTR-3B (monthly summary and tax payment)

- GSTR-9 (annual return)

- Input Tax Credit (ITC) can be claimed on eligible purchases.

Compliance with DTAA Provisions

India’s DTAAs with 90+ countries help avoid double taxation.

- Useful for reducing withholding tax on cross-border payments.

- Documentation (TRC, Form 10F, etc.) must be maintained and submitted.

Other Local Taxes and Levies

The subsidiary may also face local taxes based on location/operations, such as:

- Professional Tax (on salaries, varies by state)

- Customs Duty (on imports)

- Stamp Duty (on agreements, capital issuance)

- Equalisation Levy (on digital payments to foreign vendors)

Labour Law & Employment Compliance for Indian Subsidiary of Foreign Company

When a foreign company sets up a subsidiary in India and hires staff, it must follow India’s complex labour laws, which ensure fair treatment and employee rights.

Shops and Establishments Act Registration

All Indian subsidiaries must register under the state-specific Shops and Establishments Act within 30 days of starting operations.

This law governs working hours, leave, holidays, and termination. Periodic renewal of the certificate is required.

Employees’ Provident Fund (EPF) Compliance

Subsidiaries with 20+ employees must register with the EPFO under the Employees’ Provident Funds and Miscellaneous Provisions Act, 1952.

Both employer and employee contribute 12% of basic wages monthly. Timely payments and electronic return filings are mandatory.

Employees’ State Insurance (ESI) Compliance

ESI provides employees with medical, maternity, and disability benefits.

If the company has 10+ employees (earning below ₹21,000/month), ESI registration is required

Contributions total 4% of wages (3.25% employer, 0.75% employee), covering medical and other benefits.

Professional Tax (PT)

Applicable in certain states (e.g., Maharashtra, Karnataka), PT must be deducted from salaries and paid to the state.

Rates vary by state; some states like Delhi do not impose PT.

Payment of Gratuity

Under the Payment of Gratuity Act, 1972, companies with 10+ employees must pay gratuity to staff completing five years of continuous service.

It equals 15 days’ wages per year of service, payable on resignation, retirement, or death.

Statutory Bonus

Payment of Bonus Act, 1965 mandates companies with 20+ employees must pay an annual bonus (8.33% to 20% of annual salary) to eligible employees earning up to ₹21,000/month, subject to profitability.

Maternity Benefit Compliance

The Maternity Benefit Act, 1961 requires companies with 10+ employees to provide 26 weeks of paid maternity leave, with full wage payment and job protection during leave.

Sexual Harassment Compliance (PoSH Act)

Applies to firms with 10+ employees.

Requires a PoSH policy, Internal Committee, annual training, and reporting to authorities. Non-compliance risks legal action.

Employment Contracts and Offer Letters

Every employee should receive a formal contract or appointment letter covering job details, salary, leave, termination, and confidentiality.

Non-compete clauses are generally unenforceable.

Leave Policies

Generally governed by the Shops & Establishments Act or Factories Act, depending on the nature of the business.

Typically include:

- Earned Leave: 15–30 days/year

- Sick Leave: 7–12 days/year

- Casual Leave: 7–12 days/year

Labour Welfare Fund (LWF)

In certain states, employers and employees must contribute to LWF for welfare programs. Contributions are small but mandatory.

Minimum Wages & Payment of Wages Compliance

Wages must meet or exceed state/central minimum wages and be paid on time (usually by the 7th or 10th of the next month). Unauthorized deductions are prohibited.

Factories Act (For Manufacturing Units)

Manufacturing units must comply with safety, sanitation, work hours, and licensing rules under the Factories Act, 1948.

The Act also regulates working hours, overtime, and employment of women and young persons

Labour Law Recordkeeping and Audits

Maintain registers for attendance, wages, leave, and salary slips. Regular audits help ensure compliance and prepare for inspections.

Sector-Specific Compliances for Foreign Company Subsidiaries

In addition to the above, Indian subsidiaries must meet industry-specific regulations enforced by sectoral regulators.

Financial Services & NBFCs

- Must register with RBI as an NBFC.

- Comply with net owned fund (NOF) requirements, capital adequacy norms, and periodic RBI filings.

- Subject to RBI inspections and restrictions on public deposits.

Insurance Sector

- Requires IRDAI license for insurance/reinsurance operations.

- Must meet solvency, capital, and ownership norms.

- Regular financial and operational reporting required.

- FDI limits and promoter background checks apply.

IT & IT-Enabled Services (ITES)

- STPI registration offers tax benefits.

- Must comply with the Digital Personal Data Protection Act, 2023 (DPDPA) for data privacy, breach reporting, and consent.

- Appoint Data Protection Officer (DPO) if handling sensitive data.

Pharmaceuticals & Medical Devices

- CDSCO/DCGI approval required for drugs and devices.

- Must obtain manufacturing/import licenses under the Drugs and Cosmetics Act.

- Clinical trials need CDSCO and ethics committee approvals.

- FSSAI license needed for food/nutraceutical products.

Telecommunications & OTT

- DoT licenses required (e.g., Unified License, ISP License).

- Comply with security rules, interconnection norms, and revenue sharing.

- OTT platforms must follow IT Rules, 2021, including grievance officers and compliance reports.

Manufacturing & Industrial Projects

- Environmental Clearance (EC) under EIA 2006 for specific industries.

- Consent to Establish/Operate from State Pollution Control Board.

- Factory License under Factories Act if employing 10+ (with power) or 20+ (without power).

- Import Export Code (IEC) for foreign trade.

- BIS Certification for regulated products.

E-Commerce & Online Marketplaces

- Must comply with Consumer Protection (E-commerce) Rules, 2020:

- Transparent seller info, return/refund policies, non-discriminatory treatment.

- 100% FDI allowed in Marketplace Model (automatic route); FDI prohibited in Inventory Model.

- Must follow Legal Metrology Rules for product labelling (MRP, manufacturer, date, quantity).

Key Differences in Compliance Requirements for Wholly Owned & Partly Owned Subsidiary

| Aspect | Wholly Owned Subsidiary | Partly Owned Subsidiary |

| Shareholding Reporting | Only Form FC-GPR (foreign investment) | Form FC-GPR + FC-TRS for share transfers |

| Board Composition | Mostly foreign-appointed; 1 Indian resident required | Mixed board; Indian partners may appoint directors |

| Corporate Governance | Simple; aligned with parent only | Requires shareholder agreements, minority rights |

| FDI Approvals | Easier under automatic route | May need sector-specific or JV-related approvals |

| Taxation | Indian tax rules apply | Same; but RPTs and accounting can be more complex |

| Related Party Transactions | Mostly with parent → focus on transfer pricing | Includes Indian entities → needs strict board approval |

| Compliance Filings | Standard company filings | May include extra disclosures for Indian shareholders |

| Profit Repatriation | 100% to parent post-tax & FEMA rules | Split as per share ratio; more steps involved |

| Event-Based Compliance | Fewer, since shareholding rarely changes | More frequent due to potential stake transfers |

| Ease of Compliance | Simple structure, faster decisions | More complex due to shared ownership |

| Legal Liability | Limited to subsidiary | Same, but minority rights increase legal oversight |

Sample Compliance Checklist for Indian Subsidiary of Foreign Company

Here’s a sample compliance checklist for Indian subsidiaries of foreign companies covering all major areas of compliance.

However, you should customize it on the basis of size, sector, and location. Reach out to our experts for a FREE initial consultation: