Expert verified

Expert verified Running a business means dealing with taxes. With these practical tips for accurate tax computation for Indian enterprises, you’ll not falter.

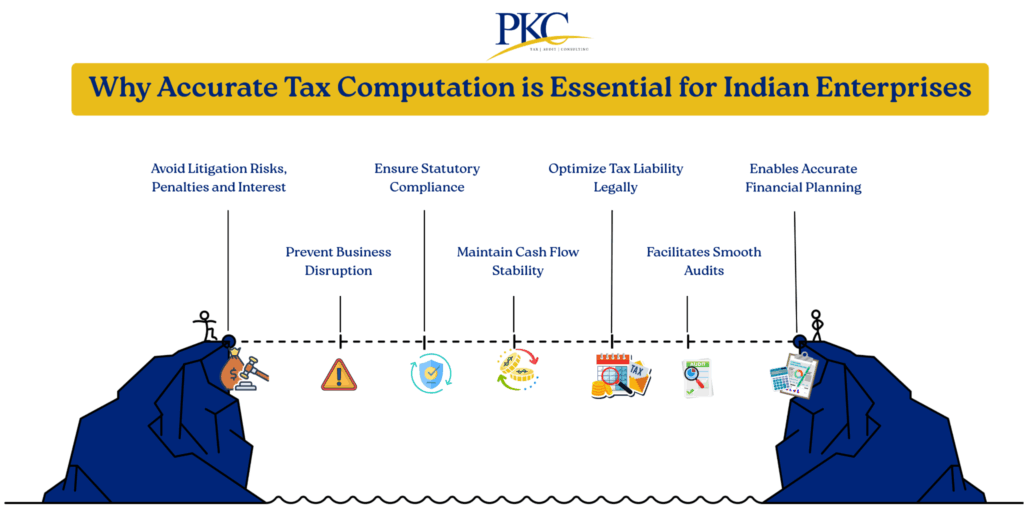

We share with you some of the most essential tips that companies in India can use to calculate their tax liability.

How to Accurately Calculate Tax for Indian Companies?

Here’s a look at how you can make your income tax calculation as a business easier:

Foundation and Record Keeping

- Maintain Detailed and Updated Financial Records

Keep comprehensive documentation of all financial transactions, including invoices, receipts, bank statements, and accounting ledgers.

Digital record-keeping ensures better organization and retrieval. Maintain backup copies and implement regular data validation processes to prevent discrepancies during tax computations.

- Maintain Clear Separation of Personal and Business Finances

Establish distinct bank accounts, credit cards, and financial systems for business operations.

This separation prevents confusion during tax calculations and ensures accurate deduction claims. Mixed finances can lead to disallowed expenses and penalties.

Income and Expense Management

- Classify Income and Expenses Correctly

Categorize different types of income (business income, capital gains, other sources) and expenses (revenue vs capital expenditure) according to Income Tax Act provisions.

Proper classification ensures that you accurately calculate your tax liability and prevent disputes with tax authorities.

- Identify All Sources of Income

Conduct comprehensive reviews to identify all revenue streams, including subsidiary income, dividend receipts, rental income, and foreign income.

Overlooked income sources can result in under-reporting and possible penalties.

- Track and Deduct Allowable Expenses

Identify and document expenses permissible under the Income Tax Act (e.g., Section 37, specific business deductions).

This includes operational costs, employee salaries, rent, utilities, and professional fees. Disallow personal or non-business expenses.

- Accurately Compute Capital Gains

Correctly determine holding period (STCG vs LTCG), cost of acquisition/indexation, exemptions (54, 54EC, 54F), and applicable tax rates for asset sales.

Maintain detailed records of asset acquisition costs, improvement expenses, and sale proceeds to ensure accurate tax computations for your business.

Why PKC is A Top Choice for Tax Filing for Enterprises? ▫️1,500+ enterprise clients trust PKC tax expertise ▫️200+ dedicated tax professionals ensure accurate filing ▫️Specialized corporate tax planning reduces enterprise liabilities ▫️Multi-entity tax filing for complex corporate structures ▫️Tech-enabled automation streamlines filing processes ▫️Real-time MIS reports for tax decision making ▫️GST integration with income tax planning ▫️Same-day filing capabilities for urgent deadlines ▫️Cost optimization strategies maximize enterprise tax savings |

Tax Structure and Rates

- Use the Correct Tax Rates for Your Business Structure

Apply appropriate tax rates based on your business entity type (sole proprietorship, partnership, LLP, private limited company, public limited company).

Different structures have varying tax implications and rates that directly impact overall tax liability.

- Understand and Apply the Correct Tax Regime

Choose between the old tax regime (with deductions) and new tax regime (lower rates without most deductions) based on your specific financial situation.

Analyze both options annually to determine the most beneficial approach for your enterprise.

- Section 115BAA vs 115BA Analysis

If applicable, deeply analyze the benefits and conditions of opting for these special lower tax rate regimes (22% + surcharge & cess) vs. the regular corporate tax rate.

Consider the trade-offs between lower tax rates and forfeited deductions.

- MAT vs Regular Tax Calculation

Calculate both Minimum Alternate Tax (MAT) and regular tax liability to determine the higher amount payable.

Maintain MAT credit records for future utilization when regular tax exceeds MAT in subsequent years.

Technology and Automation

- Automate Tax Computations with Software

Implement reliable tax software solutions that can handle complex calculations, ensure compliance with current tax laws, and reduce human errors.

Automated systems provide consistency and generate audit trails for tax computations.

- Perform Tax Scenario Modeling

Use financial modeling tools to project different tax scenarios based on various business decisions, investment options, and strategic choices.

This helps in making informed decisions that optimize tax efficiency.

Compliance and Updates

- Stay Updated on Amendments

Regularly monitor changes in tax laws, notifications, and circulars issued by the Income Tax Department.

Track evolving digital tax rules—like equalization levies, digital service PE rules, and tax treaties—that impact digital businesses.

Subscribe to official publications and professional tax services to stay informed about amendments that affect your tax computations.

- Keep Track of TDS and Advance Tax

Track Tax Deducted at Source (TDS) credits and ensure timely payment of advance tax installments.

Maintain records of TDS certificates and calculate advance tax liability accurately to avoid interest charges.

- Ensure Quarterly Compliance

Meet all quarterly compliance requirements that include advance tax payments, TDS returns, and other periodic obligations.

Prepare a compliance calendar to track due dates and avoid penalties.

Deductions and Incentives

- Accurately Apply Tax Deductions and Exemptions

Claim all eligible deductions under various sections of the Income Tax Act while ensuring proper documentation and compliance with conditions.

Common deductions available for businesses include business expenses, depreciation, and specific industry incentives.

- Explore Sector-Specific Incentives and Deductions

Research and utilize tax incentives available for your specific industry, such as manufacturing incentives, R&D benefits, or export promotion schemes.

These significantly reduce your effective tax rate.

- Track Depreciation Methods

Apply appropriate depreciation rates and methods for different asset categories as prescribed in the Income Tax Act.

Maintain detailed fixed asset registers and ensure consistency in depreciation calculations across financial years.

- Consider Presumptive Taxation Where Applicable

Evaluate eligibility for presumptive taxation schemes under Sections 44AD, 44ADA, or 44AE.

These can simplify tax computations for eligible small businesses and professionals.

Specialized Areas

- GST Compliance

Ensure proper GST registration, filing, and payment compliance as it impacts income computation for direct tax purposes.

Make sure to synchronise GST and income tax records.

- Transfer Pricing Documentation

For enterprises with related party transactions, maintain comprehensive transfer pricing documentation -(Master File, Local File, and CbCR as per Section 92-92F) and ensure arm’s length pricing.

This prevents adjustments that could increase tax liability.

- International Taxation Management

Handle foreign income, tax treaties, and international tax obligations carefully.

Maintain documentation for foreign tax credits and ensure compliance with reporting requirements for international transactions.

Professional Support and Auditing

- Perform Regular Internal Tax Audits

Conduct periodic checks (monthly/quarterly) to identify errors, missed deductions, or compliance gaps before external audits.

If applicable, consider your Tax Audit (Section 44AB) requirements.

- Consult Tax Professionals When in Doubt

Engage qualified tax professionals like PKC Management Consulting for complex situations, uncertain interpretations, or significant business transactions.

Professional guidance can prevent costly mistakes and ensure optimal tax planning.

- Professional Development

In case you are relying on your internal tax team, make sure to invest in their continuous learning and training.

Stay updated with latest tax developments, attend seminars, and maintain professional certifications to ensure competent tax management.

Advanced Considerations

- Factor in Rebates, Surcharges, and Cess

Calculate the complete tax liability including applicable rebates, surcharges, and cess.

These additional components can significantly impact the final tax amount.

- ESG and Sustainability Integration

Consider tax implications of Environmental, Social, and Governance (ESG) initiatives.

Some sustainability investments may qualify for special tax incentives or deductions.

Risk Management

- Contingent Liability Assessment

Evaluate and document potential tax liabilities arising from disputed assessments, pending appeals, or uncertain tax positions.

This helps in accurate financial reporting and planning.

- Tax Litigation Tracking

Maintain detailed records of ongoing tax disputes, appeals, and litigation matters.

Track deadlines and ensure proper representation in tax proceedings.

- Review and Strategize for Loss Carryforward Rules

Understand the latest rules on loss carryforwards in case of mergers or restructuring.

The recent amendments have tightened these provisions which can impact computation of taxes for businesses.

- Consider Impact of Direct Tax Code (DTC)

With the introduction of the DTC, ensure your tax planning and compliance strategies are adaptable to the new, unified tax structure.

Frequently Asked Questions

- What are the consequences of inaccurate tax filings in India?

Penalties, interest, and even prosecution can follow if taxes are miscalculated or underreported. Repeated errors may lead to audits or legal notices.

- How should companies calculate depreciation for tax purposes?

Depreciation must be calculated as per the Income Tax Act, not Companies Act. It impacts taxable income and should be done using WDV (Written Down Value) method in most cases.

- Is MAT (Minimum Alternate Tax) still applicable?

Yes, for companies claiming exemptions or deductions under the old regime, MAT at 15% of book profits may apply under Section 115JB.

- What are the tax compliance forms companies must file?

Common forms include ITR-6 for income tax, GSTR-1 and GSTR-3B for GST, and Form 26Q/24Q for TDS filings.