Expert verified

Expert verified Analysis of Section 92CE (2A) of Income Tax Act, 1961

WHAT IS PRIMARY ADJUSTMENT?

- Primary adjustment to a transfer price means determination of transfer price in accordance with the arm’s length principle

- Such adjustment results in increase in total income or reduction in the loss of the assessee.

- Such adjustment shall be made

- either Suo moto by the assessee in his return of income or

- by Assessing officer which is accepted by the assessee or

- adjustments made pursuant to Advance Pricing Agreement (APA) entered into or

- resolutions under Mutual Agreement Procedure (“MAP”) or

- upon availing safe harbor under the Act.

WHAT IS SECONDARY ADJUSTMENT (SECTION 92CE)?

- “Secondary adjustment” means an adjustment in the books of account of the assessee and its associated enterprise to reflect that the actual allocation of profits between the assessee and its associated enterprise(AE) are consistent with the transfer price determined as a result of primary adjustment, thereby removing the imbalance between cash account and actual profit of the assessee.

- Where a primary adjustment has been made to the transfer price, the assessee is required to make secondary adjustment.

- In the following cases, secondary adjustment is not required to be made:

- the amount of primary adjustment made in any previous year does not exceed one crore rupees, or

- The primary adjustment is made in respect of an assessment year commencing on or before the 1st day of April, 2016.

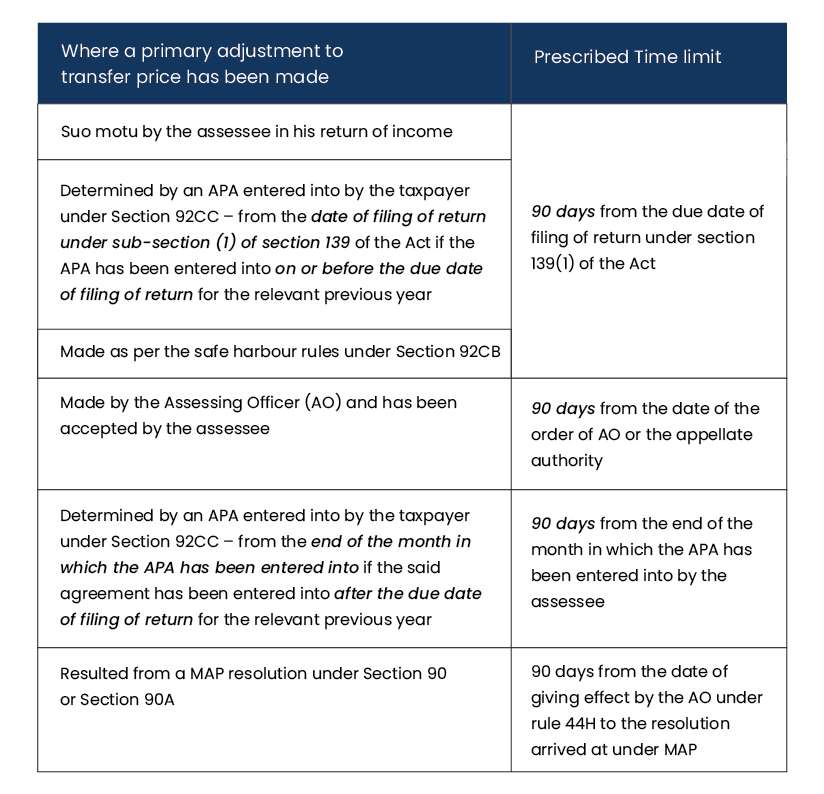

- As a result of primary adjustment, the excess money which is available with the AE, has to be repatriated to India within the prescribed time limit, which is as follows:

- The excess money can be repatriated from any of the AE of the assessee, provided the AE is a non-resident.

CONSEQUENCES IF THE EXCESS MONEY IS NOT REPATRIATED WITHIN THE PRESCRIBED TIME LIMIT:

- If the excess money or part thereof, is not repatriated into India within the prescribed time frame, the such excess money or part thereof, shall be deemed to be an advance made by the assessee to such AE and Notional Interest will be computed on such Advance.

- Manner of Computing Interest as per Rule 10CB:

- at the 1-year marginal cost of fund lending rate of State Bank of India as on 1st of April of the relevant previous year plus 325 basis points in the cases where the international transaction is denominated in Indian rupee; or

- at 6-month London Interbank Offered Rate (Libor) as on 30th September of the relevant previous year plus 300 basis points in the cases where the international transaction is denominated in foreign currency.

Interest shall be computed from the due date of filing return of income u/s 139(1) or the date of order of the AO or from the end of the month in which APA has been entered into or the date of giving effect by the AO under Rule 44H.

- Such interest will be added to the Total Income of the assessee and tax on such income has to be paid at the rate applicable to the assessee.

OPTION TO THE ASSESSEE TO PAY ONE TIME TAX:

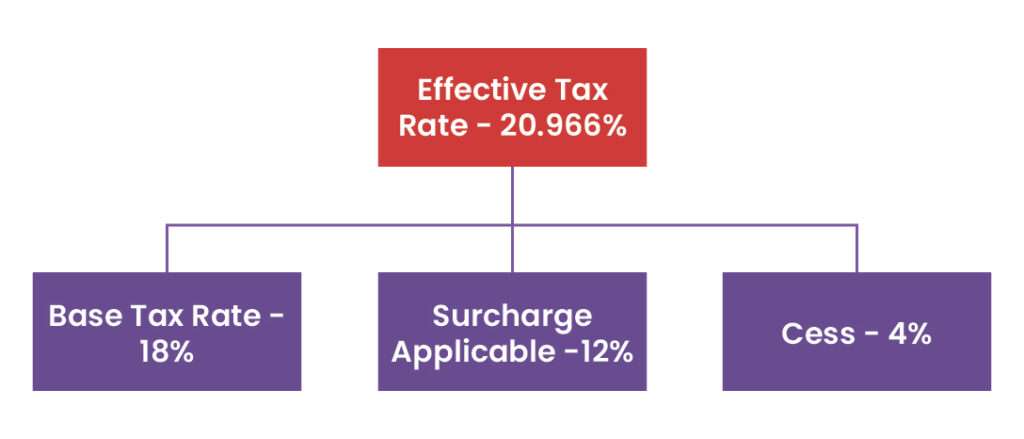

- An option is now available to the taxpayer to pay a one-time additional tax @ 18% (plus surcharge of 12% & Cess) on the un-repatriated amount,

- No credit shall be allowed in respect of the amount of such tax. Further no deduction shall be allowed under any other provision of the Act in respect of the amount on which the tax is paid.

- Where the taxpayer exercises this option, interest imputation on the said amount will cease on the date of payment of the additional tax. It is also proposed that where this additional one-time tax is paid, the assessee shall not be required to make secondary adjustment under sub-section (1) of section 92CE of the Act.

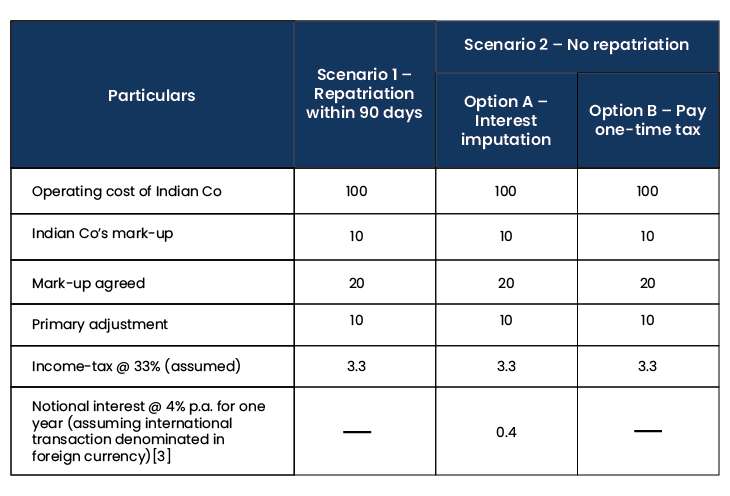

ILLUSTRATION:

An Indian IT services company provides services to its overseas AE in the US on a cost plus 10% basis and receives service fee in USD. During the course of TP audits, the Indian Revenue Authorities made a primary adjustment by asserting an operating margin of 20% on cost which was accepted by the taxpayer Group.

Income tax on notional interest for a year = 0.4*0.33= 0.13

One-time additional tax @ 20.96%= 10*0.2096= 2.10

CONCLUDING REMARKS:

- With the introduction of option to pay one-time tax, the assessee has the facility to settle all tax liability arising in India from a TP adjustment with a single payment, rather than go on imputing interest into perpetuity, providing critical relief, particularly in cases where repatriation is not possible due to exchange control regulations, AE ceasing to exist, etc. Further, the requirement to make a secondary adjustment is proposed to be removed if the option of paying one-time tax is exercised.

Also Check: 92CE Secondary Adjustment in Books