Pass Through Income (SECTION 115UA & 115UB)

Section 115UA

The taxability of the income earned by Business Trust is governed by Section 115UA of the Income tax Act, 1961.

WHAT IS A BUSINESS TRUST?

Section 2(13A) of Income Tax Act defines Business Trust as below:

“business trust” means a trust registered as, —

(i) an Infrastructure Investment Trust under the Securities and Exchange Board of India (Infrastructure Investment Trusts) Regulations, 2014 made under the Securities and Exchange Board of India Act, 1992 (15 of 1992); or

(ii) a Real Estate Investment Trust under the Securities and Exchange Board of India (Real Estate Investment Trusts) Regulations, 2014 made under the Securities and Exchange Board of India Act, 1992 (15 of 1992)

These trusts are like mutual funds that raise resources from many investors to be directly invested in real estate projects or infrastructure projects. The income-investment model of REITs and InvITs (referred to as business trusts) has the following distinctive elements:

- the trust would raise capital by way of issue of units (to be listed on a recognized stock exchange) and can also raise debts directly both from resident as well as non-resident investors;

- The income bearing assets would be held by the trust by acquiring controlling or other specific interest in an Indian company (SPV) from the sponsor.

.

NOTE: The important amendment made by Finance Act, 2020 in definition of Business Trust is that the business trusts earlier can recognized only listed InvITs and REITs registered with SEBI but now it includes unlisted InvITs and REITs registered with SEBI as well. This amendment will take effect from April 1, 2020.

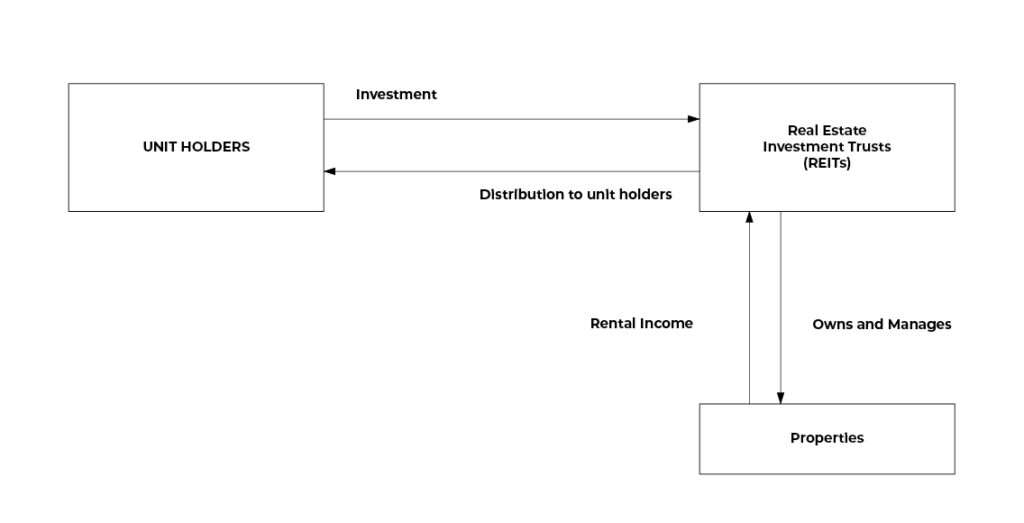

HOW DOES A REIT WORK?

Real Estate Investment Trust (REIT) is a trust that owns and manages income generating developed properties and offers its unit to public investors. REITs own many types of commercial real estate, ranging from office and apartment buildings to warehouses, hospitals, shopping centers, hotels and even timberlands.

Globally, REITs invest primarily in completed, revenue generating real estate assets and distribute major part of the earning among their investors. Typically, most of such investments are in completed properties which provide regular income to the investors from the rentals received from such properties.

- REITs are principally expected to invest in completed assets. Income would consist of rental income, interest income or capital gains arising from sale of real assets / shares of SPV.

- REITs are managed by professional managers which usually have diverse skill bases in property development, redevelopment, acquisitions, leasing and management etc.

- Listed REITs provide liquidity, thus providing easy exit to the investors.

Investment

Distribution to unit holders

Rental Income Owns and Manages

INFRASTRUCTURE INVESTMENT TRUSTS (InvITs)

Infrastructure Investment Trusts make direct investment in infrastructure facilities which are yielding income e.g. Toll Road, Railways, Inland waterways, Airport, Urban public transport. InvITs will allow infrastructure developers to monetize specific assets, helping them use proceeds for completing projects of theirs stalled for want of funds.

Structure of InvITs is quite similar to REITs. The main difference is InvITs make investment into infrastructure facilities whereas REITs make investment in commercial real estate properties.

TAXABILITY U/S 115UA:

In the hands of the Unit holders

The income of unit holders of Business Trust can be categorized into two parts.

- Tax on Income Distributed by Business Trust

There is a special taxation regime for taxability of income distributed by such business trusts in the hands of the unit holders. The income distributed by a business trust to its unit holders shall be deemed to be of the same nature and in the same proportion in the hands of the unit holders, as it had been received by, or accrued to the business trust.

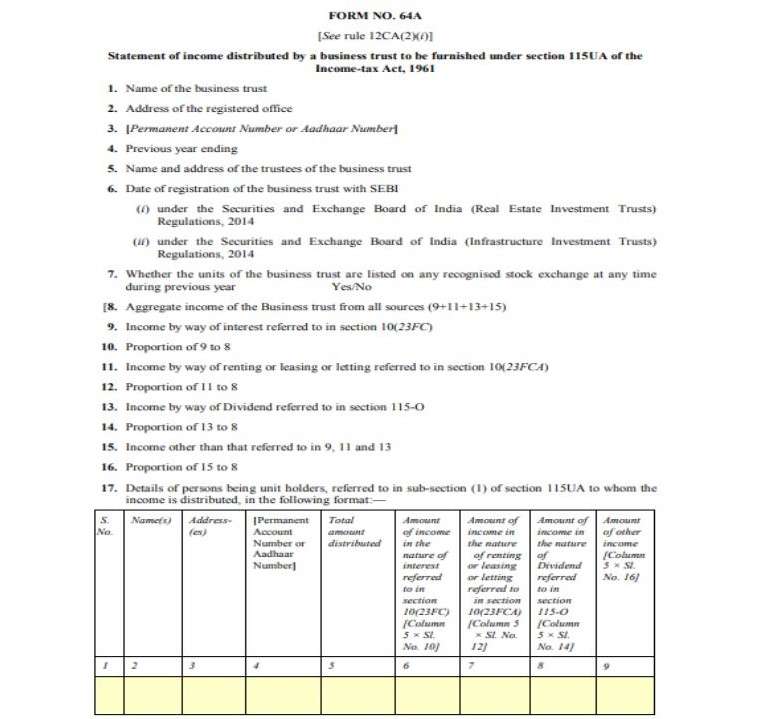

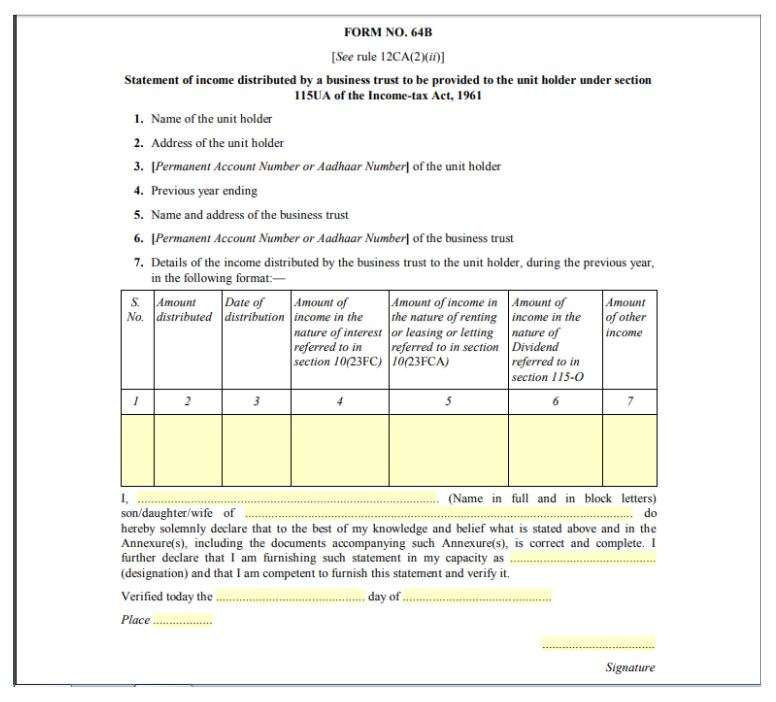

The person distributing the income on behalf of the business trust is required to furnish the statement of income distributed to the unitholder in Form No. 64B by the 30th June.

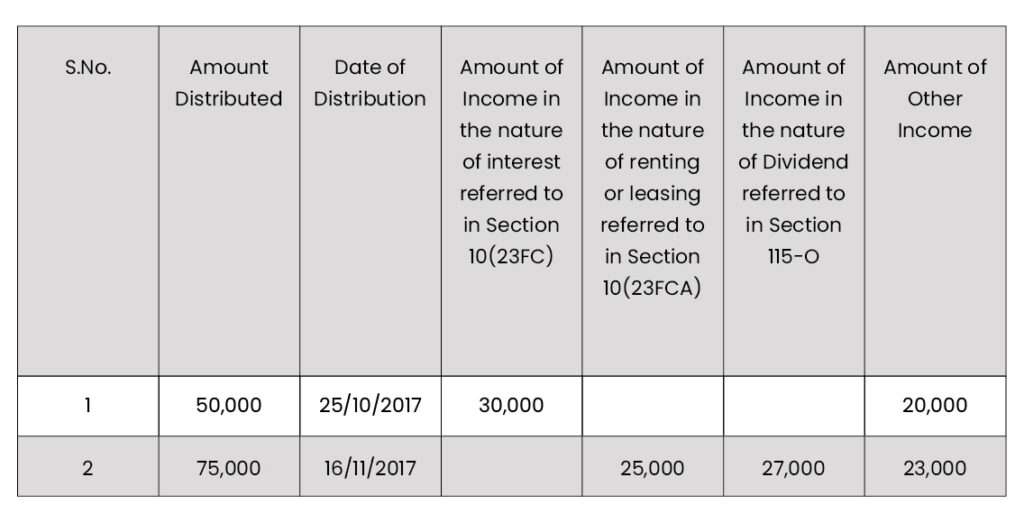

Example, Mr. Arun, a resident individual, has received the following ‘Form 64B – Statement of income distributed by a business trust to the unit holders’ for the Financial Year 2017-18.

Let’s see how taxability of each of such income will be determined in the hands of Mr. Arun.

Income in the nature of Interest

The income in the nature of interest referred to in sub clause (a) of Section 10(23FC) is chargeable to tax in the hands of the unit holders. If the unit holder is non-resident the rate of tax on such income is 5% and for resident unit holders, it is chargeable to tax at slab rates.

This income is exempt in the hands of the business trust. This interest received or receivable from a special purpose vehicle by the business trust is accorded a pass-through treatment and is taxable directly in the hands of the unit holders. The business trust is liable to deduct TDS on this interest income at the rate of 10% in the case of a resident unit holder and 5% in the case of Non-resident unit holders.

Example, Mr. Arun has to include the income of Rs. 30,000 distributed by the business trust on 25/10/2017 as an interest income in his Income Tax Return.

Rental Income

The rental income referred to in Section 10(23FCA) is taxable income in the hands of the unit holders.

Any income of a business trust, being a real estate investment trust, by way of renting or leasing or letting out any real estate asset owned directly by such business trust is exempt in the hands of the business trust. This income is chargeable to tax in the hands of the unit holders as rental income. The REIT is liable to deduct TDS on such distributed income at the rate of 10% for resident unit holders and at the rates in force for non-resident unit holders.

Example, Mr. Arun has to show the income of Rs. 25,000 distributed on 16/11/2017 by the business trust as rental income in his Income Tax Return.

Dividend Income

This dividend component of the income distributed by the business trust is exempt in the hands of the unit holder. The business trust is also provided an exemption in respect of such income. However, with effect from April 1, 2020, there has been an overhaul of India’s dividend tax regime. Until now Indian companies were required to pay DDT and shareholders (except non-corporate residents) were exempt. Going forward, the tax incidence will shift from the company to the shareholders.

In case of business trusts, dividends used to be exempt at each level (albeit subject to some conditions), however, as part of the new dividend taxation regime, the government did not announce any relief specific to the investors in business trusts in its Budget tax proposals

Any Other Income

Any distributed income, referred to in section 115UA, received by a unit holder from the business trust is exempt in the hands of the unit holder as per Section 10(23FD)

Example, The income of Rs. 20,000 received on 25/10/2017 and Rs. 23,000 received on 16/11/2017 is exempt in the hands of Mr. Arun.

2. Tax on Income on Sale of Units

The profit from the sale of the units of the business trust is chargeable to tax under the head capital gains. The tax treatment will differ for the Short-term capital gains and long-term Capital gains. The period of holding of units of the business trust to qualify as a long-term capital asset is more than 36 months.

Short-Term Capital Gain

The short-term capital gains on which STT is paid is chargeable to tax at the rate of 15% as per section 111A. The deductions under Chapter VI-A are not allowed from such capital gains.

Long-Term Capital Gain

The long-term capital gains on which STT is paid were exempt in the hands of the Unit holders under Section 10(38) till the A.Y 2018-19.

Exemption for long-term capital gains arising from the transfer of units of business trust has been withdrawn by the Finance Act, 2018 w.e.f. Assessment Year 2019-20 and a new section 112A is introduced in the Income-tax Act.

As per Section 112A, long-term capital gains arising from the transfer of a unit of a business trust shall be taxed at 10% (without giving the benefit of indexation). The tax on capital gains shall be levied in excess of Rs. 1 lakh. The deductions under Chapter VI-A are not allowed from such capital gains.

In the hands of the business trust:

REITs have been conferred as hybrid pass-through status for income tax purposes, meaning that the onward distribution of income by a REIT to its unit holders retains the same character as the underlying income stream received by the REIT. Interest income and rental income from property held directly by the trust, is not taxable in the hands of the REIT. However, any capital gains on the sale of assets/ shares of an SPV are taxable in the hands of the trust, depending on the period of holding whereas dividend income is not liable to tax. Further, any other income earned by a REIT shall be subject to tax at the maximum marginal rate.

Business trust is compulsorily required to file return as per section 139(4E)

SUMMARY:

| Nature of Income Distributed | In the hands of Business Trust | In the hands of Unit Holders |

| Interest received or receivable from a Special Purpose Vehicle | 10(23FC) provides exemption for the Business Trust | Taxable under the head IFOS |

| Income by way of renting or leasing out any asset owned by such Business Trust | 10(23FCA) provides exemption for the Business Trust | Taxable under the IFHP |

| Dividend | 10(23FC) provides exemption for the Business Trust | Taxable under the head IFOS |

| Any Other Income | Taxable | 10(23FD) provides exemption for the Unit Holders |

Statement under sub-section (4) of section 115UA.

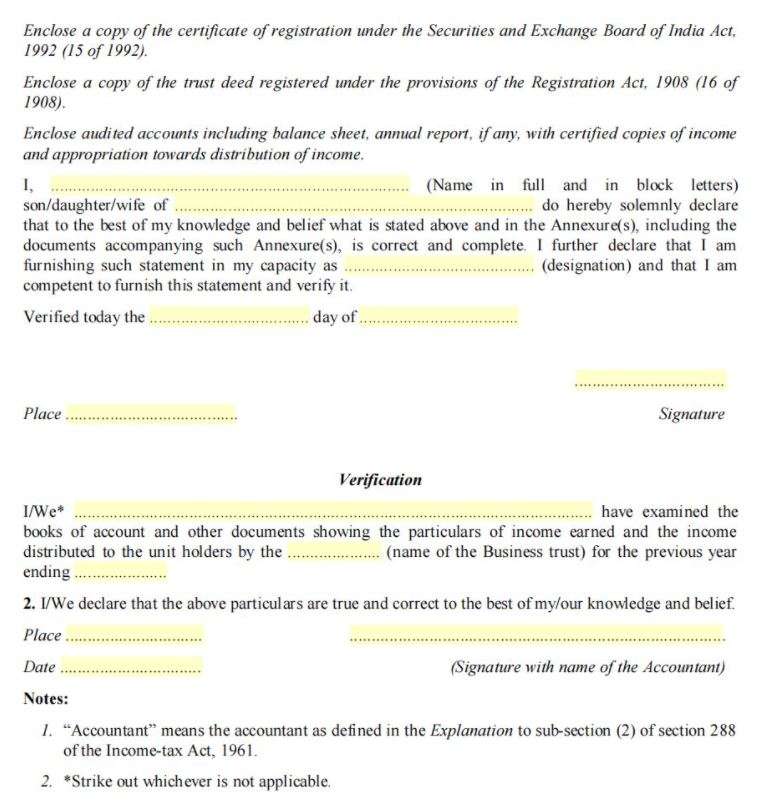

(1) The statement of income distributed by a business trust to its unit holder shall be furnished to the Principal Commissioner or the Commissioner of Income-tax within whose jurisdiction the principal office of the business trust is situated, by the 30th November of the financial year following the previous year during which such income is distributed,:

Provided that the statement of income distributed shall also be furnished to the unit holder by the 30th June of the financial year following the previous year during which the income is distributed.

(2) The statement of income distributed shall be furnished under sub-section (4) of section 115UA by the business trust to –

(i) the Principal Commissioner or the Commissioner of Income tax referred to in sub-rule (1), in Form No. 64A, duly verified by an accountant in the manner indicated therein and shall be furnished electronically under digital signature;

(ii) the unit holder in Form No. 64B, duly verified by the person distributing the income on behalf of the business trust in the manner indicated therein.

FORM 64A:

FORM 64B:

Section 115UB

The taxability of the income earned by AIF (Alternate Investment Fund) is governed by a special tax regime as provided under Section 115UB of the Income tax Act, 1961.

What is an Alternative Investment Fund (AIF)?

Alternative Investment Fund or AIF means any fund established or incorporated in India which is a privately pooled investment vehicle which collects funds from sophisticated investors, whether Indian or foreign, for investing it in accordance with a defined investment policy for the benefit of its investors.

AIF can be established in the form of a company or a corporate body or a trust or a Limited Liability Partnership (LLP).

According to the Securities and Exchange Board of India (SEBI), AIFs are classified into three broad categories:

Taxability u/s 115UB

For the Purpose of this section, Investment Fund means any registered category I & II AIF

The Indian tax law grants special tax pass through status to Category-I and Category-II AIFs. In effect, this means that the AIFs are ignored as entities for the purposes of taxation of income from investments. There is a legal presumption that the investor directly makes such investment, and, hence, the income received by the AIF is taxed in the hands of the investor, based on the tax provisions applicable to such investor. However, since legally the investment is made by the AIF entity and the income from the investment is actually received by the AIF, the law requires that the AIF withhold appropriate tax from the amount of income credited or distributed to the investor at the rates applicable to the investors. The investors are required to offer such income to tax in their annual tax returns and claim credit for the taxes withheld by the AIF. This pass-through status is not given in respect of ‘business income’ of the AIF. In case of business income, the AIF itself is taxed on it and then there is no withholding when such income is distributed by the AIF to the investor.

Previously, the AIF was not permitted to pass on its losses to the investors. This led to an anomaly where investors were being taxed on the income, but were not given benefits of losses incurred from the investments. Budget 2019 provides for pass through of losses in cases of Category I and Category II Alternative Investment Fund

Section 10(23FBA) provides exemption to an Investment fund for any income other than the income chargeable under the head “Profits and gains of business or profession”

The loss other than the loss under the head “Profits and gains of business or profession”, if any, accumulated at the level of Investment fund as on the 31st day of March, 2019, shall be, —

- deemed to be the loss of a unit holder who held the unit on the 31st day of March, 2019 in respect of the Investments made by him in the Investment fund

- allowed to be carried forward by such unit holder for the remaining period calculated from the year in which the loss had occurred for the first time taking that year as the first year and shall be set off by him in accordance with the provisions of Chapter VI:

The loss deemed to be the loss of the Unit Holders shall not be available to the Investment fund on or after the 1st day of April, 2019.

The government may also consider a tax pass through status to Category-III AIFs. Currently, the Indian tax laws do not contain any specific provisions governing taxability of Category III AIFs. Typically, these are structured as trusts and the laws governing taxability of trusts are used for determining taxability of Category-III AIFs and their investors.

Statement under sub-section (7) of section 115UB

The statement of income paid or credited by an investment fund to its unit holder shall be furnished by the person responsible for crediting or making payment of the income on behalf of an investment fund and the investment fund to the-

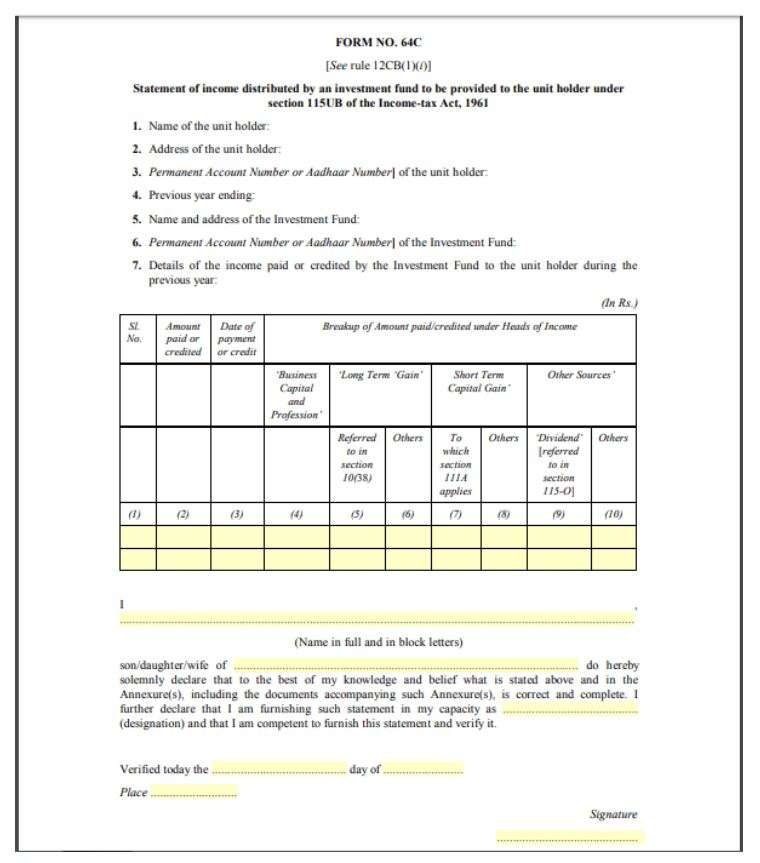

(i) unit holder by 30th day of June of the financial year following the previous year during which the income is paid or credited in Form No. 64C, duly verified by the person paying or crediting the income on behalf of the investment fund in the manner indicated therein; and

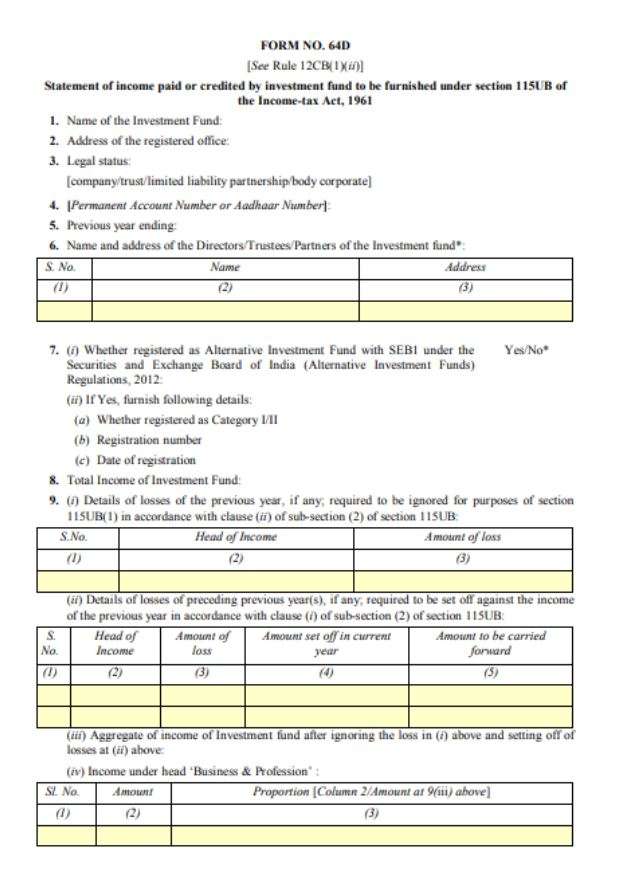

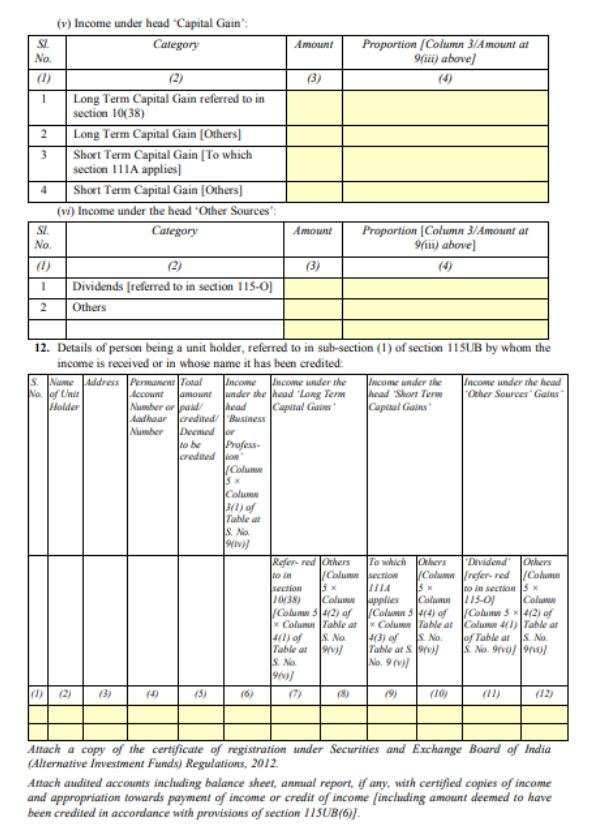

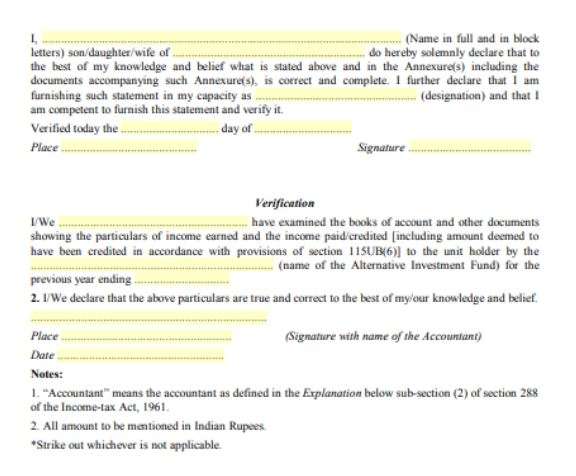

(i)) Principal Commissioner or the Commissioner of Income-tax within whose jurisdiction the Principal office of the investment fund is situated by 30th day of November of the financial year following the previous year during which the income is paid or credited, electronically under digital signature, in Form No. 64D duly verified by an accountant in the manner indicated therein.

FORM 64C:

FORM 64D:

Types of Fund

Venture Capital Fund (VCF)

Venture Capital Funds invest in Startups which have high growth potential but are facing an investment crunch in the initial phase and need funding to establish or expand their business. Since it is difficult for new businesses and entrepreneurs to raise funding through the capital markets Venture Capital Funds become the most sought-after solution for their financing needs.

VCFs pool in money from investors who want to make equity investments in ventures. They invest in multiple startups, depending on their business profiles, assets’ size, and phase of product development. Unlike mutual funds or hedge funds, venture capital funds focus on early-stage investment. Each investor gets a share of the business the VCF has invested in proportional to their respective investment.

High Net Worth Investors (HNIs) who seek high risk-high return investments options prefer to invest in VCFs. After the inclusion of VCFs in AIFs, HNIs from abroad are also able to invest in VCFs and contribute to the growth of the economy.

Infrastructure Fund (IF)

The fund invests for the development of public assets such as road and rail infrastructure, airports, communication assets etc. Investors who are bullish on the infra development in the coming times can invest in the fund since the infrastructure sector has high barriers to entry and relatively low competition.

Returns from investing in an Infrastructure Fund can be a combination of capital growth and dividend income. When an Infrastructure Fund invests in socially desirable/viable projects, the government may also extend tax benefits on such investments.

Angel Fund

This fund is a type of Venture Capital fund where fund managers pool money from numerous “angel” investors and invest in budding startups for their development. As and when the new businesses become lucrative, investors get the dividends.

In the case of Angel Funds, units are issued to the angel investors. An “angel investor” refers to an individual who wants to invest in an angel fund and brings in business management experience, thus guiding the startup in the right direction. These investors typically invest in firms which are generally not funded by established venture capital funds because of their growth uncertainty.

Social Venture Fund

Socially responsible investing has led to the emergence of Social Venture Fund (SVF) that typically invests in companies that have a strong social conscience and aim to bring a real change in the society.

These companies focus on making profits and solve environmental as well as social issues simultaneously. Even though it is a kind of philanthropic investment, one can still expect returns because the firms would still make profits.

Social Venture Fund generally invests in projects based out of developing countries as they have great potential for growth as well as social change. Such investments also bring the best managerial practices, technology and vast experience on the table which makes it a win-win deal for all stakeholders including investors, enterprises and society.

Private Equity (PE) Fund

PE funds basically invest in unlisted private companies and take a share of their ownership. Since unlisted private companies cannot tap capital through the issuance of equity or debt instruments, they look out for PE funds.

Further, these companies present their investors a diversified portfolio of equities which essentially lowers the risk to the investor. A PE fund typically has a fixed investment horizon ranging from 4 to 7 years. After 7 years, the firm expects that it would be able to exit the investment with a good amount of profit.

Debt Fund

This fund primarily invests in debt instruments of listed as well as unlisted companies.

Companies that have low credit scores generally release high yield debt securities accompanied with high risk. So companies with high growth potential, good corporate practices but facing capital crunch can be a good investment option for debt fund investors.

As per the SEBI regulations, the amount invested in Debt Fund cannot be utilized for the purpose of giving loans, as Alternative Investment Fund is a privately pooled investment vehicle.

Fund of Funds

As the name suggests, this fund is a combination of various Alternative Investment Funds. The investment strategy of the fund is to invest in a portfolio of other AIFs rather than making its own portfolio or deciding what specific sector to invest in. However, it should be kept in mind that Fund of Funds under AIFs cannot issue units of fund publicly, unlike Fund of Funds under Mutual Funds.

Hedge Fund

A hedge fund pools capital from institutional and accredited investors and invests in domestic as well as international markets to generate high returns. They take up leverage to a great extent and have aggressive management of their investment portfolio. Hedge funds are relatively less regulated as compared to its counterparts such as mutual funds and other investment vehicles.

However, they are expensive relative to other financial investment instruments. Hedge Funds generally charge 2% as the asset management fee and take up 20% of the profits earned as a fee.

Private Investment in Public Equity Fund (PIPE)

It is a privately managed pool of privately sourced funds earmarked for public equity investments. Private investment in public equity refers to buying shares of publicly traded stock at a discounted price. This enables the investor to purchase a stake in the company, while the company selling the stake receives capital infusion to grow its business.