Expert verified

Expert verified Are you overpaying taxes like most other small business owners? These tax saving tips for small business owners can be of assistance.

From registration to operational, these tax saving strategies will help you reduce your tax liability as a MSME and help you keep most of your money for future growth and sustainability.

21 Essential Tax Saving Tips for Small Business Owners in India

Let’s take a look at some of the most effective tax saving strategies for MSMEs and small businesses:

1.

Register as a MSME

Consider registering as a Micro, Small, and Medium Enterprise (MSME) in India. It offers various tax benefits including:

- May qualify for an income tax holiday for a specified number of years.

- May be eligible for a lower corporate tax rate of 25% if their annual turnover is up to INR 400 crore

- Some new manufacturing MSMEs can opt for a reduced tax rate of 15%.

- Businesses with an annual turnover below INR 1.5 crore can benefit from the GST Composition Scheme, which allows them to pay GST at a lower (fixed) rate.

- Access to various government incentives, including subsidies for technology upgrades and easier credit access at lower interest rates.

- MSME registered entities can get loans at concessional rate of interest by submitting well defined project report.

2.

Utilize Presumptive Taxation Scheme

Small businesses with less than INR 2 crores turnover can opt for this scheme under Section 44AD of the Income Tax Act.

It allows them to declare income at a fixed rate without the need for detailed accounting. This minimizes the bookkeeping requirements, simplifies tax compliance and can reduce tax liabilities.

3.

Weigh The Pros & Cons of Your Business Structure

Choosing the right business structure (Sole Proprietorship, Partnership, LLP, Pvt Ltd Company) can significantly impact your tax liability.

Each structure has different tax rates and benefits. Evaluate the pros and cons, and choose the most tax-efficient option.

Consulting a tax advisor can be helpful as they assist you with aligning your business goals and with the right structure.

4.

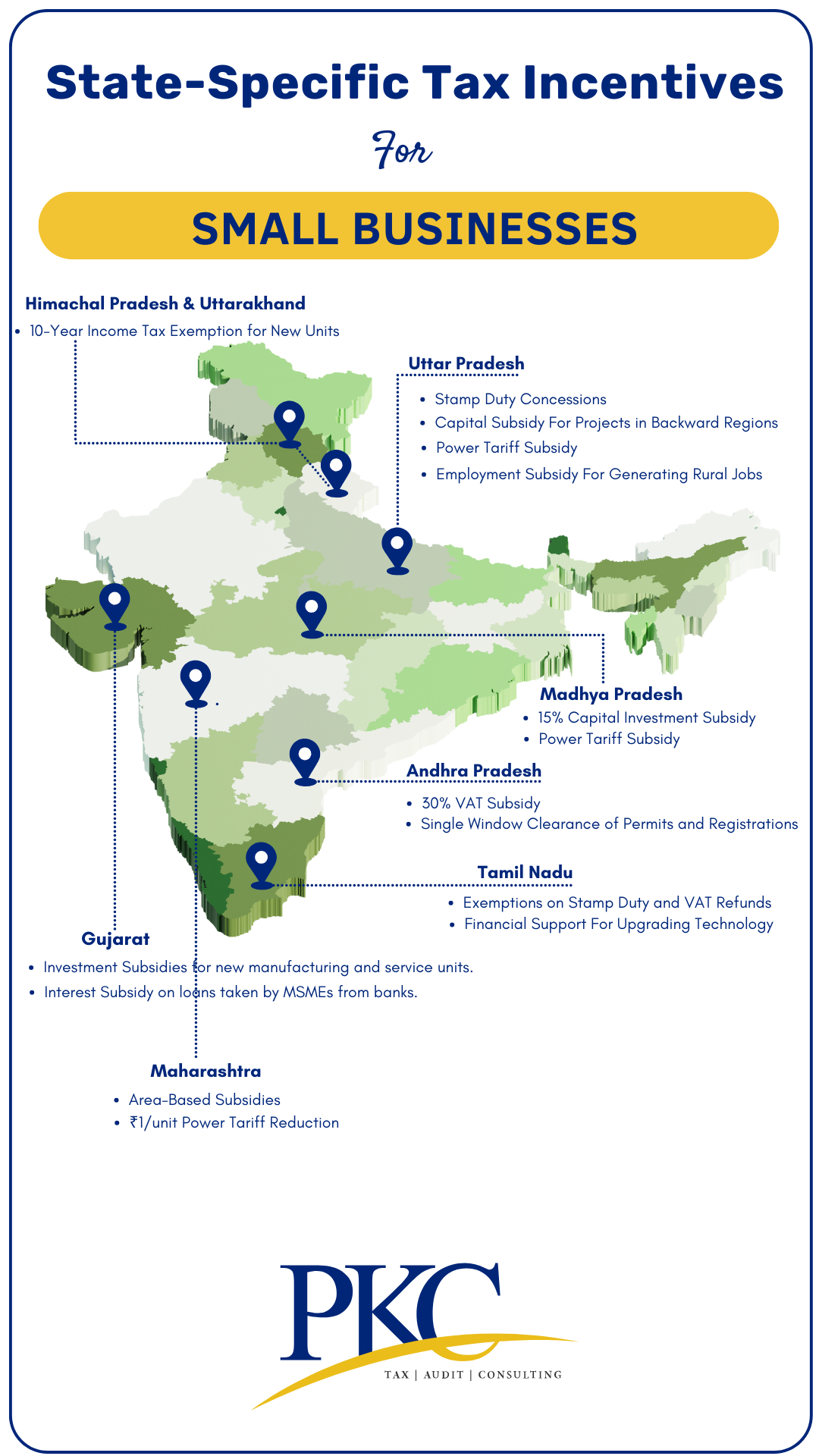

Explore State-Specific Tax Incentives

Many Indian states offer various tax incentives to promote businesses particularly for startups and small enterprises engaged in manufacturing or service sectors.

Some states provide lower tax rates or tax breaks for certain industries. Research and take advantage of these incentives.

Visit state government websites or consult local business chambers. Ensure your business qualifies for the incentive and follow the required procedures to apply for benefits.

5.

Utilize Deduction for Depreciation

Businesses can claim depreciation on assets used in their operations; it could be buildings, machinery, vehicles. etc. This helps reduce taxable income.

Understand and utilize the applicable depreciation rates for different asset categories like tangible and intangible assets.

Maintaining detailed records of asset purchases and usage and update asset registers to reflect additions and disposals.

Additionally, businesses may benefit from additional depreciation on new assets, allowing for greater upfront tax relief in the year of purchase.

6.

Avail Tax Credits – TDS & GST

Input Tax Credit (ITC) under GST allows small businesses to offset the GST paid on inputs against the GST collected on outputs.

TDS credits allow you to claim the tax deducted by clients or other entities as a credit against your tax payable.

Make sure you maintain proper records and regularly match your records with Form 26AS for TDS and GST returns.

7.

Claim Deduction for Medical Insurance

The premiums you pay for health insurance policies for yourself and employees are eligible for tax deductions.

This not only provides tax relief but also improves employee satisfaction, retention and ultimately the productivity in your business.

Note that these deductions are not claimable under the new scheme of the Income Tax Act

8.

Make Use of Tax-Saving Instruments

Investing in specific financial instruments qualifies for tax deductions, thereby reducing taxable income.

These include Equity Linked Savings Schemes (ELSS), Public Provident Fund (PPF), or National Pension System (NPS) can provide deductions.

We recommend spreading investments across multiple instruments to balance risk and returns.

9.

Implement Tax-Efficient Salary Structures

For your employees, design salary packages with tax-efficient components. It can reduce both employer and employee tax liabilities.

You can consider components like:

- House Rent Allowance (HRA)

- Leave Travel Allowance (LTA)

- Conveyance Allowance

- Company Car

- Health Insurance

- Provident Fund (PF)

- Gratuity

10.

Make Digital Payments

Making digital payments can help small businesses reduce taxable income by offering transparency and traceability of expenses.

Digital transactions are also often eligible for tax deductions. Cash transactions above INR 10,000 are disallowed as expenses by the Income Tax Department.

Plus, adopting digital payments may lead to government incentives and reduced scrutiny.

Additionally, businesses with a turnover of up to INR 10 crore can avoid tax audits if at least 95% of their transactions are conducted digitally, further streamlining compliance.

11.

Claim Interest on Business Loans

The interest paid on loans taken for business purposes is deductible from your taxable income, thereby reducing tax liability.

It is highly recommended that you keep personal and business finances distinct to simplify interest claims.

12.

Invest in Infrastructure and Technology

Investing in infrastructure and technology not only boosts your business but also offers tax deductions under various sections.

Section 35 deals with deduction for in-house R&D expenditure and software development.

13.

Carry Forward and Set Off Losses

If your business incurs losses, these can be carried forward for up to 8 years to offset against future profits.

Offsetting losses against future profits lowers taxable income in profitable years. It also provides a buffer during lean periods by utilizing past losses.

14.

Reinvest Profits

Consider reinvesting profits back into the business for promoting growth and optimizing tax liability.

Investments in business assets, infrastructure, R&D qualify for depreciation and other deductions.

15.

Call For Expert Assistance

Having an experienced service provider like PKC Management Consulting by your side, can make things smoother.

Tax experts identify and apply relevant deductions and credits you might overlook.

16.

Utilize Home Office Deductions

If you operate your business from home, you can claim deductions for a portion of home-related expenses.

Rent, utilities, internet, phone bills, maintenance, and depreciation on home office space are all eligible expenses you can claim while filing ITR.

Additionally, if you are GST registered and have a business board outside your home, ensure that it complies with GST regulations

17.

Don’t Forget to Claim Initial Business Expenses

Expenses incurred before officially starting a business may be claimed under Section 35D over five years.

This includes costs related to market research, setup, and other preliminary activities.

Note that this deduction is one-tenth of the expenditure for ten consecutive years, starting from when the business begins or the extension/new unit is operational.

18.

Utilize Deductions on Business Expenses

Every legitimate expense you incur on running a business can be deducted from taxable income.

Some of the Common Eligible Business Expenses include :

- Operational Costs: Rent, utilities, salaries, office supplies.

- Marketing and Advertising: Costs associated with promoting your business.

- Travel Expenses: Business-related travel and transportation costs.

- Professional Fees: Payments to lawyers, accountants, consultants.

- Repairs and Maintenance: Costs for maintaining business assets.

However, make sure you are keeping meticulous records to substantiate these claims during audits.

19.

Consider Family Employment

Employing family members can be a tax-efficient strategy, provided it’s done legitimately.

It shifts income within the family, potentially taking advantage of lower tax brackets.

However, ensure family members have genuine roles and responsibilities in the business.

20.

Opt for Smart Accounting Practices

This is an indirect way of saving tax for small businesses. Using efficient accounting systems helps in maintaining accurate records of income and expenses.

This minimizes errors and ensures all deductions are captured. It also provides better visibility into business finances for strategic decision-making.

You can use accounting softwares like Tally, QuickBooks, or Zoho Books for streamlined accounting.

21.

Plan for Succession and Estate

Although not a short term strategy, this can help optimize tax liabilities during the transfer of business ownership.

Proper planning can reduce or eliminate estate taxes. It also allows for smooth transition of ownership without significant tax burdens.