Expert verified

Expert verified

TL;DR SummaryTax planning and tax compliance serve fundamentally different purposes — planning is a voluntary, forward-looking strategy to legally minimize tax liabilities through deductions, income structuring, and exemptions, while compliance is a non-negotiable legal obligation focused on accurate, timely filing of returns and payments. Tax planning is measured by effective tax rate reduction and cash flow optimization, whereas compliance is measured by filing accuracy and timeliness — both require different tools, effort levels, and risk management approaches. The smartest financial strategy combines both — using professional expertise and data analytics for proactive planning, while maintaining robust record-keeping and ERP systems to stay compliant and penalty-free year-round. |

Wondering what kind of services you need, tax planning vs tax compliance. These are two essential aspects of financial management in India but differ in their approach.

Explore with us the difference between tax planning and tax compliance and see how each one works.

Tax Planning vs Tax Compliance: How They Differ?

Before we can discuss the difference between tax planning and compliance in details, here’s a quick look at their differences:

Challenges in Tax Planning

While tax planning offers significant benefits, it also comes with its own set of challenges. Navigating these complexities requires a clear understanding of evolving regulations and a strategic approach.

Some of the key challenges include:

- Complex and Evolving Tax Laws

Tax regulations are intricate and frequently updated, making it difficult for businesses to stay fully compliant while optimizing tax positions. - Multiple Jurisdictions

Businesses operating across different states or countries must deal with varying tax rules, rates, and compliance requirements, adding to the complexity. - Overlap Between Business and Personal Taxes

For closely held businesses, distinguishing between personal and business expenses and planning effectively across both can be challenging. - Risk of Non-Compliance

Inadequate record-keeping or delays in filings can lead to penalties, interest, and legal consequences. - Exposure to Tax Scrutiny

Complex transactions or aggressive tax strategies may increase the likelihood of scrutiny or audits by tax authorities. - Changing Business Environment

Business expansions, restructuring, or regulatory changes often require continuous adjustments in tax planning strategies. - Limited Internal Resources

Many businesses may not have dedicated expertise to manage tax planning effectively, leading to missed opportunities or compliance gaps.

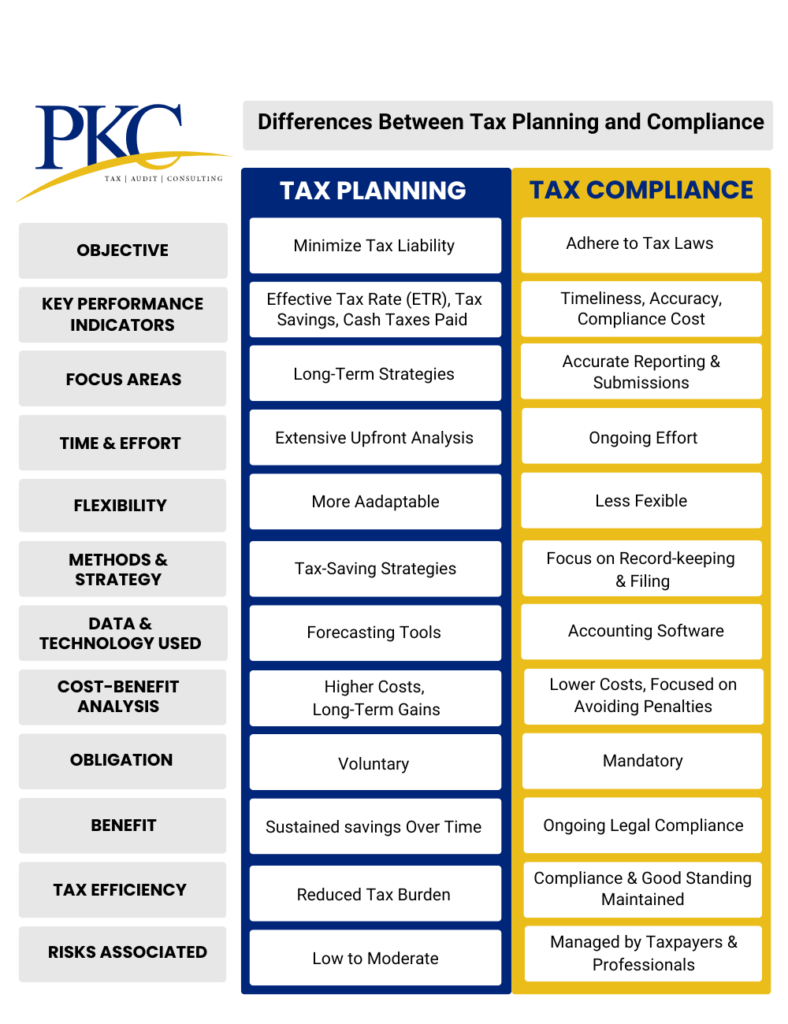

Difference in Primary Objective

The main aim of tax planning is to optimize tax liabilities. This is done using effective financial structuring, ensuring individuals or businesses pay the least amount of tax legally possible.

In contrast, tax compliance involves adhering to tax laws and regulations by accurately reporting income, expenses, and taxes owed. The goal is to avoid penalties, legal issues, or scrutiny from tax authorities.

Key Performance Indicators (KPIs)

Success in tax planning is often measured by how well individuals or businesses manage to use exemptions, deductions, and rebates.

The KPIs tax planners often use include:

- Effective Tax Rate (ETR): Measures the average rate of tax paid on pre-tax profits.

- Tax Savings: Quantifies the financial benefits gained from tax planning initiatives

- Cash Taxes Paid: Tracks the actual amount paid for taxes

Measurement of tax compliance is different and deals with fulfilling obligations.

The KPIs for tax compliance include:

- Timeliness: Measures the percentage of tax returns filed by their due dates

- Accuracy: Reflects the percentage of error-free tax returns filed

Focus Areas in Tax Planning Vs Compliance Services

Tax planning focuses on strategic areas like investment decisions, capital structuring, income splitting, and utilizing tax holidays or incentives offered by the government.

It looks forward to future financial planning and tax-saving opportunities.

Tax compliance, however, focuses on ensuring that all tax regulations (like income tax, GST, and corporate taxes) are met according to deadlines.

This includes the accurate filing of forms, submission of tax payments, and adherence to procedural obligations.

Time & Effort

Tax Planning requires significant time and effort. Tax experts will analyze financial situations and develop strategies that align with long-term financial goals.

This can involve extensive research into various investment options and understanding complex tax laws.

Conversely, tax compliance is time-sensitive and revolves around fixed deadlines, such as filing returns by the due dates.

While it may not require continuous attention, peak periods, like the end of the financial year, demand significant time and effort.

Tax compliance, however, focuses on ensuring that all tax regulations (like income tax, GST, and corporate taxes) are met according to deadlines. To see how PKC handles both ends of this spectrum, explore our comprehensive Income Tax Services — from strategic planning to accurate, on-time filing for individuals and businesses across India.

Flexibility in Compliance vs Planning

Tax Planning offers greater flexibility as taxpayers can adjust their strategies based on changing financial circumstances or new tax laws.

In contrast, Tax Compliance is less flexible. This is because taxpayers need to strictly adhere to legal requirements, and failure to comply can result in penalties or legal actions.

Methods & Strategy

Tax Planning utilizes a number of different strategies to optimize tax position for taxpayers.

This may include structuring income to benefit from lower tax rates, utilizing deductions, investment diversification, timing of income recognition, and utilization of permissible deductions.

Tax Compliance, in comparison, follows a more standardized method.

Proper methods are adopted for record-keeping, timely filing of returns, and ensuring that all forms are completed accurately according to regulatory requirements.

Data & Technology Used

Tax planning involves increasing usage of data and data analytics tools to assess financial situations and predict future liabilities effectively.

These help in estimating future tax liabilities and analyzing various investment scenarios.

In tax compliance, on the other hand, the focus is on using software to maintain accurate records, prepare returns, and file them electronically.

Compliance requires the use of accounting software, ERP systems, and digital tools to track transactions and generate reports for accurate tax filing.

Cost-Benefit Analysis

In case of tax planning, there is often an upfront cost for onboarding professional advisory services and the time invested in strategizing.

However, the long-term benefits of effective tax planning can often outweigh these costs through reduced tax liabilities and optimized cash flow.

For tax compliance, the costs are usually related to administrative expenses such as accounting fees, filing costs, and software tools for preparing tax returns.

The benefits are mostly in avoiding penalties, legal scrutiny, and interest on unpaid taxes, ensuring smooth operations.

Comparing Obligation

Tax planning is not obligatory but is recommended for anyone seeking to optimize their tax position and make sound financial decisions. It is a voluntary exercise.

Tax compliance, however, is a legal obligation. Every taxpayer must comply with the rules set by the Income Tax Department, GST authorities, and other relevant bodies, failing which may invite penalties or prosecution.

Tax Planning Vs Tax Compliance Benefit

The benefits of tax planning and tax compliance differ in focus and outcome.

Tax planning offers the advantage of reducing tax liabilities by utilizing various strategies. It also enhances cash flow, and maximizes long-term savings.

In contrast, the benefit of tax compliance lies in meeting legal obligations, avoiding penalties, fines, and audits.

Tax Efficiency

Tax Planning is fundamentally about achieving maximum tax efficiency by minimizing liabilities through strategic choices.

A well-planned tax strategy ensures that the taxpayer pays only what is required, no more, and optimally structures their finances for maximum savings.

Tax compliance, while essential, does not inherently lead to tax efficiency.

It ensures correct payment of taxes but does not focus on reducing the tax burden beyond what the law stipulates.

Risks Associated

Tax planning carries the risk of misinterpreting tax laws or the use of over-aggressive strategies that might later be disallowed by tax authorities.

Therefore, planning requires a careful balance between aggressive and conservative approaches.

Tax compliance risks include penalties, interest on late payments, or prosecution if returns are not filed properly or on time.

Non-compliance can also lead to audits, legal scrutiny, and damage to an individual’s or a company’s reputation. Whether you need help optimizing your tax position or ensuring every filing is accurate and on time, Book a FREE 30-minute consultation with PKC’s tax experts — and get a clear, actionable plan for both your planning and compliance needs.

Practical Tips to Improve Tax Planning Efficiency

To overcome these challenges and make tax planning more effective, businesses can adopt a proactive and structured approach:

- Engage Professional Expertise

Working with experienced tax advisors helps in developing compliant and optimized tax strategies. - Stay Updated with Regulations

Regularly tracking changes in tax laws ensures timely adjustments and better decision-making. - Maintain Proper Documentation

Accurate records of income, expenses, and investments are essential for claiming deductions and avoiding disputes. For a practical example of how strategic tax planning works on a specific financial decision, read our guide on How to Save Tax When Buying a Car — a real-world walkthrough of 15 legal tax-saving strategies that combine both planning and compliance - Plan Early and Review Regularly

Tax planning should be a continuous process rather than a year-end activity, allowing flexibility and better outcomes.